D&O insurance outcomes depend heavily on definitions of wrongful acts, claims triggers, and exclusion wording. Independent review and precise triggering of policy language helps executives, boards, and investors protect capital, governance strategy, and personal liability exposure.

Get Bespoke Coverage at the Lowest D&O Insurance Cost

Lowest D&O insurance cost is contractually guaranteed for similar coverage. Otherwise, we pay the difference. Applicable worldwide.

References and Testimonials on Lowering D&O Insurance Cost while Enhancing Coverage

DeshCap is referenced by Global Finance Magazine on how matching a company's risks to the language of the insurance policy can also reduce premiums.

“We cut our directors and officers insurance cost by 35% while upgrading coverage—from $50 000 to $32 500 annually—thanks to DeshCap’s independent audit.” — CFO, Mid-Cap Tech Company

👉 Book our Free Demo Call:

- Learn about our world leading tools alongside the process of designing and triggering D&O insurance wording for best cost, compliance, operational protection, financing, and valuations.

- Our engineers are licensed, AI-assisted, and broker-independent:

- Typically saving clients 10–35% on D&O insurance cost while eliminating coverage gaps that could cost far more later.

- Able to provide Full Claims Management with Cash Advance at Loss, which is outside of the purview of brokers.

- Can either manage procurements on your behalf including executing with brokers; OR provide you with analytics for your own execution.

Why Most D&O Insurance Fail Executives and Entities

Most D&O insurance policies don’t fail because of low limits — they fail because of wording.

Executives often rely on summaries, certificates, or renewal assumptions without seeing how definitions, exclusions, and claims triggers actually operate when a dispute occurs. A single sentence in the policy can determine whether a claim is fully covered, partially covered, or denied.

Common issues we see when auditing D&O programs include:

- Claims triggers that activate too late during investigations or regulatory actions

- Narrow “Wrongful Act” definitions that weaken governance protection

- Hidden endorsements added at renewal that reduce payout potential

- Over-reliance on corporate indemnification instead of true personal protection

Before committing to a full audit, you can test your policy wording instantly using the AI-Assisted D&O Policy Wording Risk Scan below.

🛡️ D&O Insurance Audit Service

A D&O Insurance Audit Service is an independent review of policy wording, exclusions, triggers, definitions, and coverage structure to determine whether a directors and officers liability insurance policy will respond as intended in actual claim scenarios.

Unlike basic quote tools or summary comparisons, an audit goes far beyond cost — it answers the central question:

Will your existing D&O policy deliver the protection your leadership team, investors, and lenders expect when a claim occurs?

What this service reviews

- Side A, Side B, and Side C coverage structures

- Definitions of “insured,” “wrongful act,” and trigger conditions

- Exclusions, carve-backs, and conditional wording

- Notice and reporting requirements

- Alignment with indemnification arrangements

- Consistency with contractual and regulatory obligations

Why it matters

Most D&O losses are not failures of limits — they are failures of wording. Narrow definitions, unintended exclusions, and ambiguous trigger language can make a policy legally non-responsive at the moment of loss, even when premiums have been paid. This audit reveals those issues before a claim arises, allowing corrective renegotiation or restructuring.

🧾 Who Needs a D&O Insurance Audit

A D&O insurance audit is an independent, structured review of directors and officers liability coverage designed for organizations that don’t just want a policy, but want confidence in how it responds in real risk events.

Boards, executives, investors, and risk leaders engage a D&O insurance audit when they want to:

- Confirm that the policy wording triggers the coverage they expect

- Identify hidden exclusions that can block claims

- Ensure Side A, B, and C structures align with governance and indemnification requirements

- Benchmark coverage against peers and best-practice triggers

- Strengthen risk position for transactions, financing, and compliance

A D&O insurance audit is especially valuable during:

- Merger and acquisition due diligence

- Investment or financing events

- Board governance reviews

- Contractual insurance obligations

- Enterprise risk management assessments

This service complements cost benchmarking by turning insurance documents into actionable risk intelligence rather than just financial inputs.

📩 Request a D&O Insurance Audit

If you are evaluating your company’s D&O risk, engaging in a transaction, or preparing for a compliance or governance event, schedule a D&O insurance audit with an independent expert.

Get an independent assessment of your D&O policy wording, coverage gaps, and structural risk exposures.

Our team works directly with boards, CFOs, general counsel, and risk committees to provide actionable recommendations and gap remediation strategies.

Explaining D&O Insurance Cost and Benchmarking

What Impacts Your D&O Insurance Cost?

- Liability Risk Score: D&O liability risk score is a function of (a) Type of entity: public, private, nonprofit; and (b) Estimated frequency and severity of D&O claims.

- Revenue & Assets: Larger balance sheets equal higher D&O insurance cost.

- Industry: Tech and healthcare firms pay 20–30% more than non-profits.

- Governance Scores: Strong ERM programs earn premium credits up to 15%.

- Claims History: Prior suits can double your rate, or more, if not expertly negotiated.

- Coverage: the breadth of coverage provided by a D&O insurance quote will directly impact cost.

- Geography: the type of jurisdiction including its legal system impacts D&O insurance cost.

- Other factors: your D&O insurance cost is driven by various other factors ranging from your operational risk profile to the state of capital markets.

Use our D&O insurance cost calculator for an instant estimate of your D&O insurance cost.

* Example of how ranges for D&O Insurance Cost are impacted by Type of Entity:

- D&O insurance cost public company: 0.25% to 5% of the D&O limit or protection amount subject to minimum premiums.

- D&O insurance cost private company: 0.05% to 3% of the D&O limit or protection amount subject to minimum premiums.

- Cost of D&O insurance for nonprofits: 0.03% to 2% of the D&O limit or protection amount subject to minimum premiums.

Elaborating on Factors Impacting Directors and Officers Insurance Cost

- The cost of officers and directors insurance depends on various factors including the nature of the company, whether it is a not-for-profit, a private company, or a public company, the size of the company, the industry it operates in, the complexity of its shareholder base and organizational charts, as well as its financial and operational performance.

- The breakdown of the cost of D&O insurance is more or less the same as that of the cost of business insurance in general.

- Typically, directors and officers insurance cost is lowest for small not for profits or small private firms with few shareholders.

- D&O insurance cost varies by country, and in the U.S. it varies by state. It is helpful to calculate cost in terms of percentage of the D&O insurance limits.

- The cost of D&O insurance also depends on the specific coverage options selected. It can be purchased as a standalone policy or as part of a broader package of insurance coverage.

- There are advanced methods to benchmark the cost of directors and officers insurance, which is most useful to mid-sized and large organizations. These methods involve the opportunity cost of self-insuring the D&O risk, which can incorporate bank financing rates.

Contact DeshCap to get the lowest D&O insurance cost with DeshCap given our contractual guarantees: we pay the difference if you have legal proof of lower cost elsewhere for similar protection.

Example: If the insurance limit is $1,000,000 and the annual premium is $10,000 then the directors and officers insurance cost would be expressed as 1%. This enables an easier comparison and benchmarking process across industries and geographies.

D&O insurance cost by Country

- D&O insurance cost in Canada is less, on average, than that in the US; it is not unusual to see the D&O premium as a percentage of the limit of liability be less than 0.1% for a CAD 1 million limit of liability in relation to organizations that are deemed to be the least risky exposure to insurance companies.

- Globally, if a company is paying over 1% in premium to insurance limit it is considered to be in the expensive range made for high risk businesses.

- D&O insurance cost will be the lowest in countries where lawsuits are not common practice, or where the judicial system is not independent or caps the amount of damages, assuming the same level of competition amongst insurance brokers and companies.

Adjusting D&O Insurance Cost To Your Profile

- Use a leading D&O Insurance Cost Calculator, such as the one above, to get an immediate feel of your premium ballpark serving as a starting point (ex. $5,000).

- Estimate the commission that is earned by your D&O Insurance Broker to get a feel of the portion of the premium that is driven purely by commissions. Discount your starting premium by a reasonable portion of such commission (ex. 5% discount to premium from reducing broker commissions: revised premium = $4,750).

- Add factors that impact your D&O Insurance Cost: unique losses or operational complexities, profile and sophistication of shareholder base, etc. Assign each factor a multiplier (ex. 1.20 adds a 20% premium to cost due to a specific factor).

- Add further debits or credits based on benchmarking with market comparable. Try to put yourself in an insurer's shoes when calculating your firm's D&O insurance cost asking yourself how much would you charge to provide adequate protection given your firm's D&O risk. As a rule of thumb, D&O insurance costs 0.03% to 5% of the protection amount or limit of liability based on the D&O risk to insurers.

- Incorporate macro economic and insurance market factors arriving at your final D&O insurance cost calculation (ex. hard vs. soft market, status of capital markets, etc.).

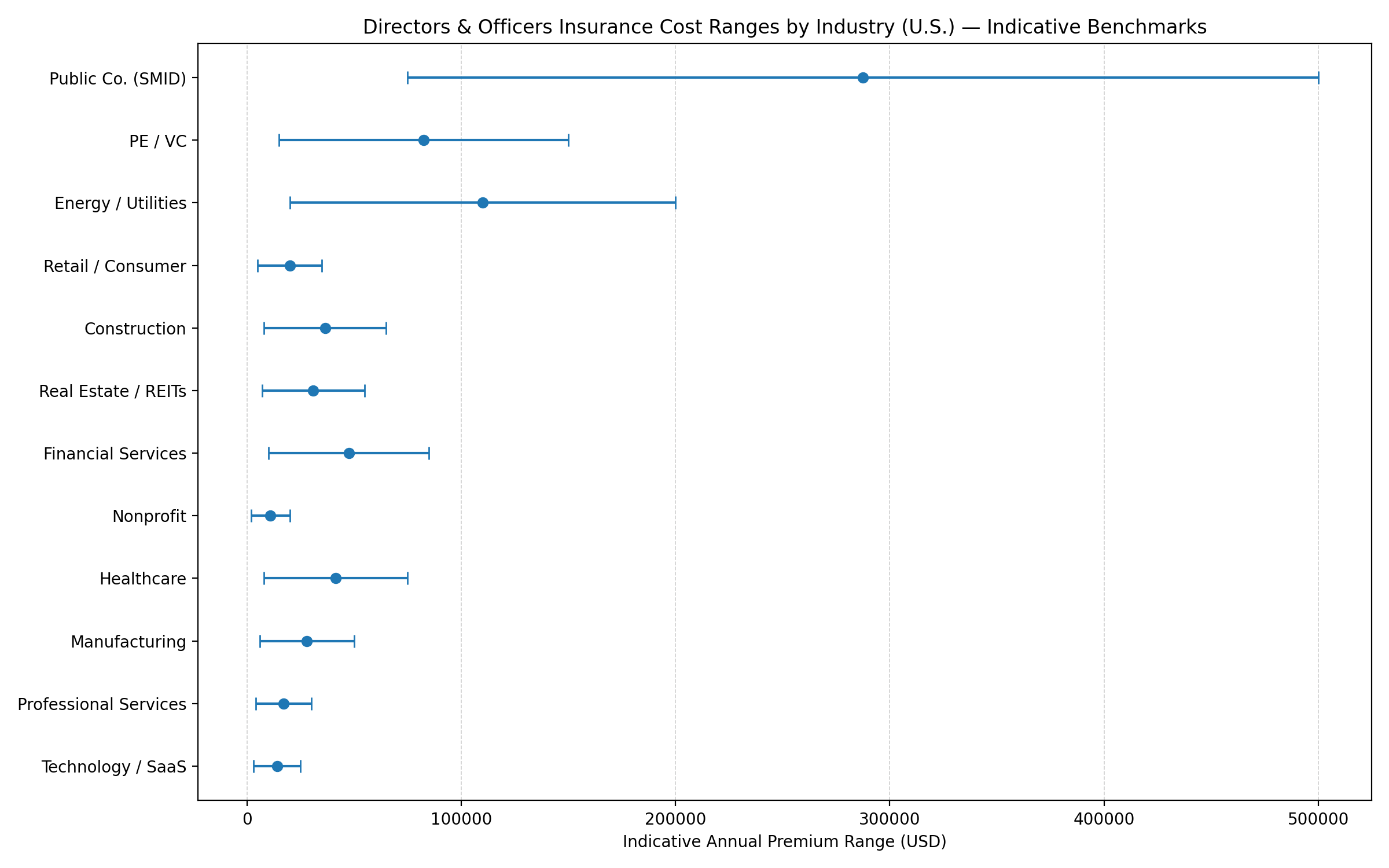

Directors and Officers Insurance Cost Based on Type of Entity

The following are ranges of D&O Insurance Cost stated as a percentage of the D&O insurance limit based on type of entity:

- Not for profit entities: Nonprofit D&O Insurance Cost = 0.03% to 2% of limit

- Private entities: Private D&O Insurance Cost = 0.05% to 3% of limit

- Public entities (listed on an exchange): Public D&O Insurance Cost = 0.25% to 5% of limit

Note that these ranges are rough indications serving as a quick guide to D&O Insurance cost based on Type of Entity. Actual D&O insurance cost and premiums may deviate from such ranges depending on the D&O risk in question. Note that the cost of officers and directors insurance is based on the same ranges.

Get the lowest Directors and Officers insurance cost given our worldwide cost contractual guarantees: if you have legal proof of lower cost for similar protection elsewhere then we pay the difference! You can also use our D&O Insurance Cost Calculator.

Cost of D&O Insurance for Nonprofits

0.03% to 2% of the limit of liability depending on the size, scope, and risk levels of non-profit organizations. Since nonprofits have no shares, there is essentially no liability risk originating from securities, which substantially reduces the cost of D&O insurance for nonprofits.

Use our D&O insurance cost calculator for an instant and more accurate indication of cost. You can also instantly purchase coverage above, which includes a contractual guarantee on lowest cost for similar protection.

Nonprofit D&O Insurance Cost Explained

Volunteer directors at charities face the same fiduciary risks as corporations—but with tighter budgets. Nonprofit D&O insurance cost typically starts under $500/year, depending on operating revenue and board size. Our independent consultants negotiate sub-$750 quotes for $1 million limits and advise on bylaws language that often mandates coverage.

As a rule of thumb, nonprofit D&O insurance cost ranges between 0.03% to 2% of the limit of liability depending on the size, scope, and risk levels of non-profit organizations. Such cost is mainly driven by the risk of employment related suits against directors and officers of the nonprofit or against the nonprofit itself.

Use our D&O insurance cost calculator for an instant and more accurate estimate of nonprofit D&O insurance cost.

Market Updates for D&O Insurance Cost

As of Q1 2026: while D&O insurance cost has been trending upwards for the last couple of years, there seems to be more entrants and competition amongst insurers which could relieve some of the cost pressure on insureds throughout 2026.

D&O insurance Quotes sold by brokers are becoming more restrictive as insurers place various coverage exclusions to their D&O insurance coverage (ex. exclusions on cyber losses that lead to lawsuits against directors or officers).

It is now easier to get a tailored D&O insurance quote through independent D&O insurance consultants such as our firm.

Example of the cost of D&O insurance in 2026

- Type of Entity: Private

- Jurisdiction: California, U.S.A.

- Industry: Technology

- Size: < $5 milion in revenue

- Limit of Liability: $2 million for Individuals shared with $1 million for the Entity

- Total D&O insurance cost: ~ $5,000

Popular Directors and Officers Insurance Cost online queries

- average d&o insurance cost

- directors and officers insurance cost uk

- d&o insurance cost uk

- hoa d&o insurance cost

- d & o insurance cost

D and O Insurance Quotes – How to Compare, Benchmark, and Reduce Cost

When evaluating D and O insurance quotes, price alone is not the determining factor. Quotes can vary significantly based on industry risk, revenue size, litigation exposure, policy wording, retention levels, and insurer appetite. Two policies with similar limits may differ materially in coverage triggers, exclusions, and payout probability.

Before selecting a D and O insurance quote, it is critical to benchmark both cost and coverage structure. The lowest premium may reflect narrower definitions of “claim,” broader exclusions, higher retentions, or restrictive allocation provisions that reduce recovery at loss.

Independent benchmarking allows businesses to:

- Compare D and O insurance quotes across multiple underwriting markets

- Identify wording gaps that affect claim payout

- Optimize retention structure without weakening coverage

- Align policy limits with governance and asset exposure

A structured review of D and O insurance quotes ensures that coverage aligns with operational risk, financing requirements, and director liability exposure — not just budget constraints.

👉 Contact DeshCap to upload your existing D and O insurance quotes for independent benchmarking and coverage analysis.

How To Procure D and O Insurance Quotes in 6 Steps

- Gather Your Corporate Details: Revenue, industry classification, previous claims history, board composition.

- Engage an Independent D&O Insurance Consultant: we audit proposed policies, remove exclusions, and negotiate premiums.

- Identify Coverage Needs: Decide on limits, retentions, Side A vs. Side B/C layers.

- Request Multiple D&O Insurance Quotes: Use our online platform to get D and O insurance quotes from providers in the U.S., Canada, U.K., and globally.

- Evaluate D&O insurance providers and coverage quoted: this is done with the help of your D&O insurance consultant.

- Bind Your Policy & Schedule Renewal Audits: Ensure your D&O insurance cost remains competitive at each renewal.

Using a streamlined and technical process on how to get D and O insurance enables the buyer to tailor coverage while minimizing D&O insurance cost with a high level of confidence.

Comparing D and O Insurance Quotes

This image is a simple illustration of how different D and O insurance quotes stack up on cost and coverage. No single D&O insurance quote is the same, and it is important to ask your D&O insurance providers for the complete sample wordings that form the basis of your D and O insurance quotes. You can also use our online insurance audit tool to get a quick and comprehensive audit of your D and O insurance quotes by experts who are independent of any broker or lobbyist.

Customize D and O Insurance Quotes at the Lowest D&O Insurance Cost Worldwide

Fill out the form below and submit it to qualify for tailored D&O insurance quotes at the lowest directors and officers insurance cost worldwide for similar protection that is contractually guaranteed: we pay the difference if you have legal proof of lower cost elsewhere.

You can also schedule our Free D&O Insurance Demo showing you how our team changes and triggers policy language for best D&O insurance cost, compliance, operational protection, financing, and valuations. Our team is independent of any insurance broker or lobbyist, working for you and not the insurer, and has skin in the game during claims.

Factors to consider when obtaining D and O Insurance Quotes

When obtaining D and O insurance quotes, there are several key factors to consider to ensure you get the right coverage at the best price:

- Policy limits: The policy limits, or the maximum amount the insurer will pay for covered claims, is a critical factor. Higher limits will provide more comprehensive protection, but they will also come with a higher directors and officers insurance cost.

How Much D&O Insurance is Needed?

- A good rule of thumb is to take the limit of insurance as a percentage of the company's assets or revenues depending on which figure is most appropriate vis a vis the industry it operates in.

- For example, for an asset manager, using Assets Under Management (AUM) to provide a quick benchmark for the D&O insurance limit is of better use than using the balance sheet asset figure.

- 1% of AUM or $1 million whichever is lower is typically the starting point for D&O limits for asset managers.

- The 1% of AUM rule of thumb can be used as a very quick way to get a ballpark figure of the D&O insurance limit up to an AUM of $1 Billion. Above the latter threshold, the correlation between AUM and D&O insurance limit breaks down.

- The limit of liability that is adequate for a specific organization and its directors and officers is one that is based on risk quantification which includes factors inherent to the organization as well as external factors such as past litigation outcomes.

- In many instances organizations are told by insurance brokers that they need to carry X amount of limit of liability because of their client benchmarking.

- However, this methodology of choosing the limit of insurance is inherently flawed because buyers usually follow their budgets or their brokers’ advice even though such advice is not data driven nor based on science, so in essence the benchmarks themselves are flawed.

- It is highly recommended for any buyer to take the advice of risk experts who are independent of insurance brokers or companies when it comes to choosing the amount of insurance that they would need to buy.

- Deductibles: The deductible, or the amount the insured must pay before the insurance coverage kicks in, can also impact the premium. Lower deductibles typically result in higher directors and officers insurance cost, while higher deductibles can lower the overall cost of the D and O insurance quotes.

- Coverage exclusions: It's important to carefully review the exclusions in the policy, as they can limit the scope of coverage. Some common exclusions include intentional acts, criminal or fraudulent conduct, and claims related to pollution or environmental issues. Remember that changing exclusions will directly impact directors and officers insurance cost.

- Reputation and financial stability of the insurer and broker: When comparing quotes, it's essential to consider the financial strength and reputation of the insurance provider. You want to ensure that the insurer will be able to pay out claims if needed.

- Industry-specific considerations: Certain industries, such as financial services or healthcare, may face unique risks that require specialized D&O coverage. Be sure to choose a policy that is tailored to your industry's needs.

- Company size and structure: The size and complexity of your organization can also impact the D&O insurance coverage you require. Larger companies with more complex structures may need higher limits and more comprehensive coverage.

By carefully considering these factors, you can ensure that you obtain the right D&O insurance coverage at a fair and competitive directors and officers insurance cost.

Get D and O Insurance Quotes instantly or use our world leading D&O insurance cost calculator for an instant cost estimate.

Clarifying Misconceptions of D and O Insurance Quotes

- The construct of Directors and Officers Insurance (D and O insurance) is around 95% Operational and 5% Legal;

- The average D&O insurance payout ratio on large losses is < 25% if not reworded clinically by independent experts;

- D&O insurance protects an entity and its subsidiaries as well as directors and officers against certain Liability Risk;

- The role of insurance brokers prohibits them from being active in a claims process and having skin in the game.

In addition to the above main points, there are several common misconceptions that can prevent organizations from obtaining the coverage they need. Understanding and addressing these misconceptions can help ensure that you make the best decision for your company.

- "My company is too small to need D&O insurance": This is a common misconception, as companies of all sizes can face lawsuits and claims against their directors and officers. Even small and medium-sized businesses can benefit from the protection provided by D&O insurance.

- "Our organization is not at risk of litigation": While some companies may feel that they are not at risk of legal action, the reality is that the business landscape is becoming increasingly litigious. Lawsuits can arise from a wide range of issues, from financial mismanagement to employment practices, and no organization is immune.

- "D&O insurance is too expensive": While D&O insurance can be a significant expense, the cost of not having coverage can be much higher. The legal fees and potential settlements or judgments associated with a lawsuit can quickly exceed the cost of a D&O policy, putting the personal assets of directors and officers at risk.

- "Our general liability or other business insurance policies will cover D&O-related claims": This is a common misconception, as general liability and other business insurance policies typically do not provide the same level of protection as a dedicated D&O policy. These policies may have exclusions or limitations that leave directors and officers vulnerable.

- "Our organization's bylaws or indemnification agreements will protect our directors and officers": While these measures can provide some level of protection, they are not a substitute for D&O insurance. Lawsuits can still be filed, and the organization may not have the financial resources to fully indemnify its directors and officers.

By understanding and addressing these misconceptions, you can ensure that your organization is adequately protected and that your directors and officers have the coverage they need to make informed decisions without fear of personal financial consequences.

D and O Insurance Quotes Offered by Online Brokers

Buying D&O insurance from an online broker should be restricted only to those organizations that are looking to check the box for certain regulatory requirements or contractual obligations.

There will be no or little opportunity to reword the D&O insurance policy for it to be meaningful from a risk management standpoint when buying from online sources, which can also lead to an inflated D&O insurance cost.

For organizations that are keen on risk management including compliance, which is yet to be automated, it is best to go through a risk expert who is independent of any insurance broker or company.

If you are looking for a D&O quote, feel free to contact us.

Explaining D and O Insurance Using World-leading Analytics

D and O insurance is a type of commercial insurance that provides financial protection for the individual directors and officers of an organization as well as the organization itself as a legal entity in case of liability tied around any alleged or actual mismanagement acts.

In essence, D&O insurance coverage is a hedge against a specific set of loss scenarios related to liability risk, it is also known as Directors and Officers Insurance or Management Liability insurance.

One important consideration is that the organization and its directors and officers may not be at fault but can still be subject to lawsuits or monetary demands that are frivolously launched against them, which would be covered through well tailored D and O insurance.

🔍 Want expert guidance on D&O Insurance? Contact DeshCap today to ensure you’re fully protected and optimizing costs!

The Main Coverages of D&O Insurance

There are three main coverage areas within a typical D & O insurance policy:

1. D&O Side A coverage, which offers protection for Ds and Os in case they are targeted or named in a lawsuit all while their company is either unable or unwilling to indemnify them for associated costs;

2. D&O Side B coverage, which offers protection for Ds and Os in case they are targeted or named in a lawsuit however while their company is able and willing to indemnify them for associated costs;

3. D&O Side C coverage, which offers protection for the company itself as a legal entity in case it is targeted or named in a lawsuit whether alongside individual directors and officers or not.

It is important to note that coverage of D&O insurance includes defence costs, indemnities, as well as other expenses, and the insurance policy should clearly define the types of expenses that are covered as well as how they are paid by the insurance company along with a timeline for such payment. Note that the policy itself will have various definitions, exclusions, and terms and conditions impacting coverage.

It is therefore of high importance for the D&O policy fine print to be audited word by word and reworded in order for relevant loss scenarios tied to liability risk be covered, as opposed to loss scenarios that cater to an insurance company’s original intent of the wording, which will also positively impact D&O insurance cost through the elimination of non essential or irrelvant coverages.

Note that each insurance company uses its own terminology whether in the form of insurance policy section titles, definitions, or exclusions and other terms. This typically adds confusion to insurance brokers as well as the buyers.

Important D&O Insurance Policy Definitions

The following are keywords that are found in the Definitions section of a D&O insurance policy and that should be analyzed in conjunction with the buyer’s needs:

CLAIM; WRONGFUL ACT; LOSS; DAMAGES; INSURED.

It is important to review and/or reword any other definition introduced by an endorsement to the D&O policy that directly impacts coverage for a core risk relevant to the buyer. This will also reduce D&O insurance cost by streamlining the operational intent of such definitions.

Do not forget to ask your insurance broker for a copy of the complete wording including all endorsements, you can also have our team perform a D&O Insurance Audit.

D&O Insurance Coverage for Lawsuits

A D&O policy can cover a range of different types of lawsuits brought against individual directors/officers or the organization itself or any of its related entities, which includes payouts for defence costs, indemnities, and other expenses incurred throughout a lawsuit.

A plaintiff can also use their D&O insurance coverage strategically in settlement negotiations or throughout the course of litigation.

It is important to reword the policy that gets sold by a D&O insurance broker to effectively cover the loss scenarios that are relevant to the organization (as opposed to those that the insurance company wants to cover).

Insurance Risk, aka basis risk, which is the risk of the insurance not paying out as expected, is a real issue within D&O coverage. It is therefore important to minimize such insurance risk and be aware of the business insurance claims process, which many business and investors tend to overlook.

What is Excluded from D&O Insurance?

There are various D and O insurance exclusions, such as:

- Illegal or fraudulent activities

- Bodily injury or property damage

- Liabilities arising from employment practices or ERISA (Employee Retirement Income Security Act) claims

- Liabilities arising from environmental or pollution incidents

- Liabilities arising from the company's financial performance or financial products

- Liabilities arising from the company's pension plan

- Fine and penalties imposed by government authorities

Here are additional real life claims that were excluded by D and O insurance policies:

· A loss that happened before an agreed upon retroactive date of the policy

· A fraud or malicious conduct that was proven to be intentional

· A loss that was covered under a different type of commercial insurance policy (ex. pollution liability, bodily injury, property damage, etc.)

· An insured who was legally pursuing another insured under the policy that had an Insured vs. Insured exclusion

More Information on D&O Insurance Exclusions

- Exclusions within a D&O insurance policy differ from one insurance company to another even though there are some common exclusions that are standard within the insurance industry as mentioned above.

- Each exclusion should be reviewed and/or reworded in order for the D&O insurance policy to be tailored to the buyer’s profile.

- This can only be done when the insurance coverage is reviewed to match the specific relevant loss scenarios of the buyer.

- The wording of D&O insurance exclusions directly impacts D&O insurance cost.

What happens most of the time is that the buyer takes the advice of an insurance broker who is compensated to sell the D&O insurance policy.

Even though some brokers show buyers that they are able to amend the insurance through endorsements, most of the time such endorsements have no real statistical impact on the core liability risk faced by the directors and officers as well as the entity itself.

D and O Insurance by Entity Type

Public Entity D&O Insurance

Public D&O Insurance (Directors and Officers Insurance for publicly traded companies) provides critical financial protection for executives against lawsuits related to their managerial decisions.

Unlike private company D&O insurance or nonprofit D&O insurance, which cover a broader range of claims, public D&O policies are primarily focused on securities-related lawsuits, such as shareholder litigation, regulatory investigations, and SEC violations.

This higher litigation exposure makes public D&O insurance significantly more expensive, with higher premiums and retentions compared to private or nonprofit coverage. The cost is driven by frequent and severe claims, as publicly traded companies face greater scrutiny from shareholders, regulators, and activist investors.

Recent trends indicate that securities class actions remain a major risk, with an increasing number of claims filed against publicly traded firms, particularly in sectors like technology, finance, and healthcare.

When purchasing public D&O insurance, businesses should focus on policies that provide comprehensive protection for securities claims, strong defense cost coverage, and favorable settlement terms to safeguard their executives from personal financial loss.

The following illustration shows how D&O risk measures are dynamic and can be changing constantly even if the underlying operations have not changed. Public D&O insurance must be updated accordingly, ideally alongside quarterly earnings.

Tailoring D&O Insurance For Public Companies

Since public companies that are listed on an exchange entail a broader type of Liability Risk, the D&O insurance cover should be reworded to include a broad range of loss scenarios that are more relevant to publicly traded companies such as:

· Higher odds of class action lawsuits;

· The public rallying of investors by law firms looking to profit from suing the company.

Typically, an abrupt downward swing or a persistent downward trend in a company’s stock price would prompt law firms to rally investors for a class action lawsuit against the company. That is why D&O insurance for public companies requires deeper analytics and attention.

D&O Insurance For Private Companies

While frequency and severity of D&O claims are less for private companies than public companies, there is a wide range of D&O insurance offerings for private companies depending on the size and nature of the business being insured.

In many jurisdictions private company D&O claims are mostly driven by employment claims (ex. employees suing directors, officers, and the company itself for workplace issues whether driven by compensation, harassment, wrongful termination, or other).

It is therefore not uncommon to see many insurers tie employment practices liability insurance to their D&O insurance coverage offering in one policy.

Directors and Officers Insurance For Nonprofits

Since nonprofits do not have shares, the securities risk within the D&O risk of a nonprofit is nonexistent, which makes D&O insurance for nonprofits one of the most profitable lines of business within commercial insurance as a whole.

- Most nonprofit D&O claims arise from employment practices (ex. harassment suits, wrongful dismissal, etc.).

- A well-tailored directors and officers insurance policy gives nonprofit leaders the confidence to make bold decisions while protecting their personal assets. It also helps attract qualified board members by reducing personal liability fears.

- No two nonprofits are alike—and neither should their D&O insurance be. Investing in the right directors and officers insurance for nonprofits ensures your leadership is protected as your mission evolves.

👉 Looking for nonprofit-specific D&O guidance? Read our Directors and Officers Insurance for Nonprofit Organizations guide.

📌 Get tailored D and O insurance quotes for your nonprofit operation.

More Knowledge of D&O Insurance

Directors and Officers Insurance Coverage Benefits

Directors and Officers insurance offers essential protection for executives against claims arising from decisions made while managing a company. Key benefits include coverage for legal defense costs, settlements, and judgments resulting from lawsuits alleging mismanagement, breach of fiduciary duty, or regulatory noncompliance.

This type of insurance not only safeguards the personal assets of directors and officers but also helps attract top leadership talent, as candidates value protection from financial risks. With D & O insurance, businesses ensure continuity and confidence in their leadership teams, minimizing the impact of costly legal disputes. Whether you operate a public company, private business, or nonprofit, D & O insurance is a crucial safeguard in today’s complex regulatory and litigation environment.

It is important to use deep legal analytics, such as the Stanford Securities Litigation Analytics, in addition to accurately measuring the D&O risk of an Insured, to structure and trigger directors and officers insurance coverage with the highest level of insurance payout ratios.

Entity Benefit of Directors and Officers Insurance Coverage

The insurance can also protect the company itself, as a legal entity, in case of liability risk against it. It is recommended to buy D & O insurance when a company is first formed and then reviewed and updated as the company grows and evolves. Public companies are typically required to have D & O insurance as part of their liability protection. Note that some lenders view D & O Insurance limits as part of a company's balance sheet.

Does D&O Insurance Cover Former Directors?

YES, it does. However just like any desired coverage it is important to ensure that it is clearly stated within the insurance policy. Many D&O insurance policies would cover past directors for up to three or four years from them having left the insured company.

Does D&O Insurance Cover Employees?

It depends, let’s break down this question into two parts.

Part 1 is the question of whether an employee of an entity that gets sued will be protected under a D&O insurance policy.

The answer is YES, the policy should certainly include employees as part of the definition of Insured or Insured Persons since this can easily be done by many insurers and is standard practice for them. Each insurance company has their own way of wording the D&O insurance policy, so it is important to review it word by word.

Part 2 is the question of whether Ds & Os would be covered under a D&O insurance policy in the event of a lawsuit brought about by an employee.

The answer is IT DEPENDS. Various insurance companies include employment practices liability insurance coverage as an add-on to their D&O insurance coverage, so buyers should make sure of such add-on if they want employment related suits covered.

It is equally important to analyze the wording provided by the employment practices liability insurance coverage in order to ensure desired coverage is met.

D&O Insurance for Investors

Robust D&O insurance, which is one of many products of investment insurance, signals strong governance, in addition to stronger balance sheet protection, to Investors such as VCs and PEs, as well as lenders.

Lower D&O insurance cost —combined with a high-payout ratio and tailored coverage— can reduce your discount rate by 50–100 bps, boosting your valuation by 5–10%. It can also reduce your financing rate by up to 25bps.

Risks Hedged Through D&O Insurance Coverage

It is important to measure the risks an organization faces and that can be covered by D&O insurance at least annually (or quarterly for some entities), which includes measuring the probability of occurrence of such risks as well as their impact amount if such risks were to materialize.

The final impact amount would have to be adjusted for D&O Insurance that is purchased and the extent to which such insurance protects individual directors and officers, as well as the organization itself.

The Elements of Best D&O Insurance

When selecting the best D&O insurance, businesses must look beyond price alone to find a policy that balances cost-efficiency, regulatory compliance, operational protection, and financial impact. A top‐tier D&O program should:

- Minimize Cost

- Competitive Premiums: Leverage independent consultants to solicit bids from multiple brokers, ensuring you secure the lowest market rates.

- Optimal Retentions & Deductibles: Tailor retentions to your risk tolerance, reducing upfront premiums without sacrificing essential coverage.

- Maximize Compliance

- Regulatory Alignment: Ensure policy wording reflects the latest SEC, SOX, securities regulations, etc., eliminating gaps that could invalidate claims.

- Governance Best Practices: Insurers often reward organizations with strong board charters, audit committees, and risk management frameworks through discounted rates.

- Enhance Operational Protection

- Broad Coverage Triggers: Confirm “Side A,” “Side B,” and “Side C” provisions are clearly defined to protect individual executives, corporate reimbursement, and entity liabilities.

- Full Defense Cost Coverage: Avoid sublimits on investigation and defense expenses, ensuring your board can mount a vigorous defense without eroding policy limits.

- Boost Financing & Valuations

- Investor Confidence: Demonstrating a robust D&O program reduces perceived governance risk, lowering the cost of capital and improving loan or equity financing terms.

- M&A & Exit Readiness: Acquirers and IPO underwriters favor companies with clean, comprehensive D&O histories—translating into higher valuations and smoother transactions.

By partnering with an independent D&O insurance consultant, organizations gain expert policy audits, bespoke endorsements, and proactive claims‐trigger management. This conflict‐free approach ensures your D&O insurance program truly ranks among the best D&O insurance solutions—delivering the ideal blend of affordability, compliance, operational resilience, and enhanced corporate value.

Linking D & O Insurance to Corporate Governance Insurance

- It is important to tailor D and O Insurance Quotes to incentivize talented management and board of directors while enhancing their effectiveness.

- On a basic level, such insurance would provide protection enabling Management and the Board to make bold decisions without fearing for ensuing personal liability.

- It is important to highlight to Management and the Board that bad faith behaviour or intentional fraudulent conduct can be excluded from the D & O insurance provided to them in order to dissuade them from such behaviour.

- D&O coverage can be tailored to an entity's corporate governance, including HR policies and management compensation, and can therefore shape the way Management and the Board interact and make decisions, impacting the long-term strategy of such entity.

- Learn more about the intricacies of director and officer liability and within the context of corporate governance based on legal research published by the likes of the American Bar Association (ABA).

Insurance D&O Coverage: Why Independent Expertise Matters

Insurance D&O coverage—short for Directors and Officers Liability Insurance—is a vital safeguard for business leaders. It protects executives, board members, and even the organization itself from personal financial loss due to claims of mismanagement, breach of fiduciary duty, regulatory violations, and more.

But selecting the right D&O insurance coverage is not a one-size-fits-all process. Proper structuring is key—and this is where independent D&O insurance consultants such as DeshCap become indispensable.

*Why Insurance D&O Coverage Must Be Structured Correctly*

Improperly structured D&O insurance can lead to dangerous gaps, such as:

- Inadequate policy limits for evolving risks like cyber liability or ESG issues.

- Poorly defined exclusions that block legitimate claims.

- Coverage voids in cross-border or merger/acquisition scenarios.

A strong policy isn’t just about having coverage—it’s about triggering that coverage when it matters most.

*The Role of Independent D&O Insurance Consultants*

Independent D&O insurance consultants specialize in designing policies that are tailored to your organization’s specific risk profile—not influenced by carrier incentives. Their value includes:

- Unbiased assessment of your existing D&O insurance coverage

- Customized structuring of policy layers, limits, and endorsements

- Claims guidance to help trigger coverage effectively at the time of loss

- Benchmarking against peers to identify coverage gaps

- Liaising directly with underwriters to secure favorable terms

Because they’re not tied to a single broker or insurer, independent consultants work in your best interest—ensuring comprehensive coverage and smooth claim execution.

Why Insurance D&O Coverage Is a Strategic Investment

Executives today face increasing personal liability from shareholders, regulators, employees, and more. Having robust, expertly structured insurance D&O coverage is not just risk management—it’s leadership protection.

And with the support of an independent D&O insurance advisor, organizations can ensure:

- Faster, fairer claims handling

- Stronger protection against new and emerging risks

- Confidence that leadership decisions are covered and defensible

📌 Key Takeaway: Don’t just buy D&O insurance—optimize it. With tailored insurance D&O coverage and guidance from an independent consultant, your organization can protect its leadership, attract top talent, and stay resilient in times of crisis. Get tailored D and O insurance quotes for your operation today.

History of D&O Insurance

D&O stands for directors and officers. D&O insurance was created right after the 1929 economic crash because many company directors and officers at that time were being subject to lawsuits due to their companies’ failures. Such individuals had to incur out of pocket expenses to defend themselves and to settle lawsuits against them. The insurance industry saw it as an opportunity to create a new product of which objective would be to financially protect the individual directors and officers in case they were brought to court or faced any sort of litigation.

With that said, the breadth of coverage offered by D&O insurance today is very different than what it was back in the 30s. The product went through various changes and evolved around meeting regulatory requirements as well as requirements from directors and officers themselves or their legal representatives given past experiences and court rulings.

Part of the evolution was also due to increased competition within the insurance industry amongst insurance brokers and companies leading to more offerings in terms of what D&O insurance would cover. For example, it is now standard practice for D&O insurance to protect the company, as a separate legal entity, that is represented by the individual directors and officers, which was not the case back in the 30s.

Moreover, D&O insurance cost has been steadily decreasing over time due to insurer profitability, which has invited more insurers over time to offer D&O coverage. With that in mind, let's dive deeper into what D&O insurance covers.

Why Directors and Officers Face Personal Liability

The evolution of regulatory bodies throughout history brought about major considerations for directors and officers, such as the following:

- Fiduciary duties

- Regulatory enforcement

- Shareholder actions

- Employment claims

- Insolvency risk

Also, the likes of the U.S. Department of Justice (DOJ) play a direct and increasingly aggressive role in director and officer liability, especially in cases involving:

- Corporate fraud

- False disclosures

- Antitrust violations

- Corruption and bribery

- Healthcare and financial crimes

- Failure of corporate oversight

Unlike the SEC, which is primarily civil and regulatory, the DOJ brings criminal enforcement actions—often targeting individual executives and board members, not just companies.

D&O Liability Insurance vs E&O Insurance

D&O Liability insurance is meant to cover losses that stem out of alleged or actual mismanagement of a specific company. Whereas E&O insurance, also known as professional liability insurance, is meant to cover losses that stem out of alleged or actual negligence in the course of providing a service to clients. In fact, the majority of D&O policies exclude E&O type claims.

It is possible to get D and O insurance quotes that provide partial E&O coverage, however that will increase the overall cost of officers and directors insurance.

Think about Liability Risk as having hundreds if not thousands of loss scenarios (ie. an entity can be sued for many different reasons, and each of these reasons constitutes a specific loss scenario). There is no single insurance product that would hedge against all loss scenarios. Instead, insurance companies offer different products, each of which can be used to cover a specific set of loss scenarios if structured and managed correctly.

D&O Insurance For Financial Institutions

Financial Institutions (FIs) are different from a risk management standpoint because their Operational Risk has a high correlation with their financial risk, whether it’s credit risk, investment risk, or market risk, depending on the type of financial institution (ex. Operational Risk in Banks).

Since Liability Risk is a part of Operational Risk, the former naturally has a higher correlation with financial risk as it relates to financial institutions. That is why the D&O insurance for Financial Institutions should be analyzed, reworded, and managed by independent risk experts with advanced financial backgrounds, and using a different set of tools than would otherwise be used for D&O insurance provided to non-FIs.

In addition, D&O insurance for venture capital firms must contemplate portfolio company D&O risk and can be incorporated within IRR. The same applies to D&O risks and insurance for private equity firms.

D&O Insurance For Startups

D&O Insurance for Startups is essential for young companies seeking to protect founders and executives from personal liability arising from management decisions, yet traditional broker-driven policies often fall short of a startup’s unique needs.

By engaging an independent D&O insurance consultant, startups can negotiate directly with multiple carriers to secure tailored coverage, competitive premiums, and favourable retentions—without the conflict of interest that comes when brokers are compensated by insurers.

An independent consultant not only structures policies to address compliance requirements under securities laws and investor covenants but also ensures that claims triggers are clearly defined and swiftly activated in the event of a shareholder suit, regulatory investigation, or financing dispute.

From a cost perspective, this approach minimizes unnecessary endorsements and premium loadings, freeing up critical runway capital. In terms of protection, founders gain peace of mind knowing their personal assets are shielded, while strong D&O coverage can enhance startup valuations during funding rounds by demonstrating robust risk management to investors.

Moreover, when packaged as part of a Venture Capital Insurance strategy across a portfolio of startups, tailored D&O policies can materially improve a VC fund’s IRR by lowering aggregate insurance expense, reducing contingent liabilities, and streamlining exit processes.

For any startup planning its next financing or scaling operation, prioritizing D&O insurance for startups with an independent consultant is a strategic imperative for compliance, cost-efficiency, protection, and valuation growth.

Get D and O Insurance Quotes for your startup including a contractual guarantee on lowest cost for similar protection: if you have proof of lower cost, we pay the difference!

D&O Insurance For Individuals

D&O Insurance for Individuals is a specialized policy designed to protect the personal net worth of executives, board members, and officers who face unique liabilities arising from corporate governance decisions.

D&O insurance for individuals must be carefully tailored—selecting appropriate protection amounts, deductibles, and policy wording to align with each insured’s personal financial plan.

High-net-worth individuals should work with an independent D&O insurance consultant to ensure the policy includes robust defense-cost provisions, clear “side A” coverage for personal assets, and favorable terms on severability and prior acts.

An independent consultant—unaffiliated with any broker or insurer—can negotiate multiple quotes, secure the most competitive cost of officers and directors insurance, and review endorsements to eliminate restrictive exclusions. When a claim arises, this consultant also guarantees that the correct provisions are triggered immediately, avoiding the delays and disputes common with standard broker-placed policies.

By investing in D&O insurance for individuals through an independent, licensed advisor, executives achieve peace of mind: their personal finances remain insulated from shareholder suits, regulatory investigations, and fiduciary liability, while preserving legacy assets and supporting long-term wealth management goals.

Get D&O Insurance for individuals instantly at a contractual guaranteed lowest D&O insurance cost for similar protection: if you have proof of lower cost, we pay the difference!

D&O Insurance For Board Members

D&O Insurance for Board Members is a critical safeguard that protects the personal net worth of individuals serving on corporate boards against claims stemming from fiduciary decisions, regulatory investigations, or shareholder lawsuits.

D&O insurance for board members must be meticulously tailored—selecting appropriate coverage limits, retentions, and “Side A” provisions that directly defend personal assets when the entity cannot indemnify.

Custom policy wording should reflect each board member’s financial planning needs, addressing prior-acts coverage, severability clauses, and entity reimbursement triggers. Engaging an independent D&O insurance consultant—completely free from broker or insurer influence—is essential to negotiate the most competitive cost of officers and directors insurance, secure favorable endorsements, and ensure claims are activated immediately upon loss. These specialists conduct detailed policy audits, identify coverage gaps, and manage endorsements to eliminate hidden exclusions.

By partnering with an unbiased, licensed consultant, board members gain peace of mind knowing their personal finances are insulated from catastrophic liabilities, allowing them to focus on effective governance without risking their legacy assets.

Get D&O Insurance for board members instantly at a contractual guaranteed lowest D&O insurance cost for similar protection: if you have proof of lower cost, we pay the difference!

A Guide to D&O Insurance HOA

Homeowners associations (HOAs) face unique governance challenges—board decisions on assessments, maintenance, and rule enforcement can lead to personal liability claims from homeowners, vendors, or regulators. That’s why D&O Insurance for HOAs is essential: it protects volunteer board members and property managers against lawsuits alleging breach of fiduciary duty, errors in contract administration, or wrongful assessments.

Unlike corporate D&O policies, HOA D&O Insurance must be tailored to community‐specific risks—such as discrimination claims, covenant enforcement disputes, and environmental compliance—and set appropriate limits and deductibles to match the association’s budget and reserve funds.

To secure the right coverage, HOAs should engage an independent D&O insurance consultant who works solely for the association, not for insurers or brokers. These consultants conduct a thorough policy audit, identify gaps—like inadequate defense‐cost coverage or exclusions for mold/remediation claims—and negotiate with multiple carriers to obtain the best cost of officers and directors insurance, as well as comprehensive terms. In the event of a claim, they ensure the correct policy provisions are triggered promptly, safeguarding board members’ personal assets and preserving the HOA’s financial stability.

By partnering with a licensed, conflict‐free D&O insurance consultant, HOAs gain peace of mind knowing their insurance program is optimized for compliance, cost‐efficiency, and maximum protection—allowing community leaders to focus on property management and resident satisfaction without exposing themselves to undue personal risk.

Get D and O Insurance Quotes for HOAs instantly at a contractual guaranteed lowest D&O insurance cost for similar protection: if you have proof of lower cost, we pay the difference!

*D&O Insurance for HOA Boards*

D&O Insurance for HOA Board members is a specialized liability policy that shields volunteer directors, officers, and property managers of homeowners associations from personal financial risk arising from board decisions.

Unlike standard HOA general liability insurance—which protects the association itself—D&O insurance for HOA Board covers claims alleging breach of fiduciary duty, wrongful assessment of dues, discrimination in covenant enforcement, or errors in financial reporting.

Because HOA boards operate under unique state statutes and face exposure to both resident litigation and regulatory fines, coverage must be carefully tailored: limits should reflect the size of the community and reserve fund, deductibles aligned with budget constraints, and policy terms explicitly include “side A” protection for individual board members when the association cannot indemnify.

To secure the optimal D&O insurance for HOA Board, it’s essential to engage an independent D&O insurance consultant. Free from any broker or insurer influence, these consultants conduct a thorough policy audit, pinpointing hidden exclusions (e.g., mold or pollution incidents) and confirming that claim triggers—such as demand letters or letters of intent—are clearly defined. They leverage competitive bidding among carriers to negotiate favorable premiums and endorsements, ensuring your HOA Board receives robust defense-cost coverage, full prior-acts protection, and entity reimbursement triggers.

In the event of a claim, an independent consultant acts swiftly to activate the correct policy provisions and advocate for the board’s interests, safeguarding personal assets and preserving the HOA’s financial stability.

By choosing a licensed, conflict-free expert to structure and manage your D&O insurance for HOA Board, community leaders gain peace of mind, compliance assurance, and cost-effective protection tailored to the governance complexities of homeowners associations.

D&O Insurance Providers

Contact us if you are looking for the right D&O insurance providers wherever your business is domiciled. There are many D&O insurance providers but choosing the right one is difficult and time consuming. Not choosing the most appropriate D&O insurance providers will increase your business risk and D&O insurance cost.

There are international D&O insurance providers (ex. AIG, Chubb, Allianz, etc.) or regional or local D&O insurance providers. They typically use their agents and/or brokers, including online platforms, to sell their off the shelf insurance.

A D&O insurance provider that has a strong brand or is well capitalized does not mean they are the right fit for specific business. Always make distinction between a provider's ability to pay versus willingness to pay. The latter is largely a function of how the fine print of coverage is worded before purchase, and triggered at loss.

Within North America, there are sources that allow you to see a list of America's Best Public D&O Insurance Providers. However such sources may not use deep analytics within their rankings. It is important to be aware of the various legal actions against D&O insurance providers, which can be accessed through sources such as Law 360 (here is a example of a recent arbitration decision for an Insured vs. Insurer involving D&O insurance).

Tips for selecting the best Directors and Officers Liability Insurance provider

Choosing the right D&O insurance provider is crucial to ensuring that your organization and its key decision-makers are properly protected. Here are some tips to help you select the best provider:

- Look for experience and expertise: Choose an insurance provider that has extensive experience in the D&O insurance market and a proven track record of providing high-quality coverage to organizations in your industry.

- Evaluate financial stability: Ensure that the insurance provider you choose is financially stable and has the resources to pay out claims if needed. Check the provider's financial ratings and review its financial statements.

- Consider the policy features: Carefully review the policy features, including the coverage limits, deductibles, and exclusions, to ensure that they meet the specific needs of your organization.

- Prioritize customer service: Look for an insurance provider that offers responsive and personalized customer service, as you'll likely need to work closely with them in the event of a claim.

- Seek out tailored solutions: Some insurance providers may offer specialized D&O insurance products that are tailored to the unique needs of your industry or organization. These customized solutions can provide more comprehensive protection.

- Negotiate the terms: Don't be afraid to negotiate the terms of the D&O insurance policy, such as the coverage limits or deductibles, to ensure that you're getting the best possible value. This directly impacts your directors and officers insurance cost.

- Consider the policy's flexibility: Look for a D&O insurance provider that offers flexible policy options, such as the ability to adjust coverage limits or add additional insured parties as your organization grows and evolves.

By following these tips, you can ensure that you select the best D&O insurance provider for your organization, giving you the peace of mind that your directors and officers are properly protected.

Benchmarking or Choosing D&O Insurance Limits

Benchmarking D&O Limits within the insurance marketplace is flawed and should not be relied on by businesses. This is because the benchmarking does not take into account the specific risk factors of each individual business that is included within the benchmarking data set.

Businesses should choose their D&O limits based on their own operational risk factors, including but not limited to the industry in which they operate, their size, operational controls and processes, financial condition, and organizational charts. Such operational risk factors impact the probability of occurrence and severity of a specific D&O loss scenario related to the organization, and that is why D&O limit benchmarking provided by brokers should not be relied on.

D&O Insurance by Jurisdiction

- United States: as one of the most litigious countries in the world coupled with the fact that D&O insurance has originated there, the U.S. dominates D&O insurance penetration rates and spend relative to other countries. The market offers a wide variety of D&O coverage options sold through broker and agents. Independent consultants are also most active in the US. Learn more about D&O Insurance USA.

- Canada: all publicly listed companies in Canada are required to carry D&O insurance and the product is therefore well known to executives. The magnitude and frequency of D&O claims in Canada is much less than in the U.S. Learn more about D&O Insurance Canada.

- Australia: thought to be one of the most litigious countries in the world, D&O insurance is a well established product in Australia.

- United Kingdom: also highly litigious relative to most other countries, the UK is home to one of the largest pools of D&O underwriters and brokers in the world. Contact us to learn more about D&O Insurance UK.

- Europe: while less litigous than the above jurisdictions, European democracies allow for due process and relaed fines.

- Other countries: the dynamics of D&O insurance, including structure, coverage, and cost, change from one country to another.

D&O Insurance News and Claims

D&O liability risk entails hundreds if not thousands of loss scenarios. It is therefore important to focus on what is relevant to the organization and its Ds & Os. Loss scenarios that can be protected against or claimed under a Directors & Officers Liability Insurance policy include monetary demands, legal investigations, or lawsuits from:

· Shareholders (including Derivative suits)

· Creditors

· Governments

· Clients

· Employees

· Service providers

· Law firms representing plaintiffs (including class action lawsuits)

The large majority of D&O claims are a result of poor financial performance.

An example of a claim that should have resulted in the D&O insurance paying out is that of Goldman Sachs directors reaching a settlement of $79.5 million to end the 1MDB shareholder suit in 2022.

How D&O Insurance Is Actually Tested in Claims

Many Insureds face issues when facing large D&O claims primarily due to coverage intent. Research and legal insights provided by entities such as Law 360 show many cases involving businesses or insureds suing brokers or insurers for failures in D&O insurance payouts (as well as payout failures from other types of commercial insurance claims).

D&O insurance denial of coverage happens even after many years of the insured purchasing D&O insurance.

We define a large D&O claim as one that meets a specific dollar threshold to the insurer, which changes from one insurer to the next and relative to the insured risk in question.

Typically small D&O claims that are 'covered' are paid fully and fast (within 90 days) by insurers as they do not represent a major challenge to their profitability, which then becomes an excellent form of marketing of such insurers. Learn more about large loss claims.

To minimize failure in D&O insurance payout, businesses should clinically audit and trigger the fine print of coverage. The D&O coverage fine print, which rarely anybody reads, should be thoroughly reviewed by a licensed commercial insurance audit consultant who is independent of any broker or insurer.

Moreover, it is important for insured to understand the commercial insurance claims process including the operational versus legal intricacies involved in coverage and claims management.

FAQ: Directors and Officers Insurance

Case studies: Lowest D&O Insurance Cost and Tailored Coverage

The importance of D&O insurance is often best illustrated through real-world case studies. Learn how a company significantly reduced its directors and officers insurance cost while enhancing coverage with this real life D&O insurance cost case study.

In addition, here are a few examples that highlight the critical role this coverage can play in protecting directors, officers, and the organizations they serve:

- The Enron scandal: The collapse of energy giant Enron in the early 2000s resulted in numerous lawsuits against the company's directors and officers, alleging financial mismanagement and fraud. Without adequate D&O insurance coverage, the personal assets of these individuals were put at risk, leading to significant financial hardship.

- The Wells Fargo account scandal: In 2016, Wells Fargo faced a barrage of lawsuits and regulatory actions after it was revealed that employees had opened millions of unauthorized customer accounts. The D&O insurance coverage helped the company and its directors and officers navigate the legal and financial fallout, providing crucial protection.

- The Volkswagen emissions scandal: When Volkswagen was caught manipulating emissions tests, the company and its executives faced a wave of lawsuits and investigations. The D&O insurance coverage helped the company manage the legal and financial consequences, ensuring that the personal assets of its directors and officers were not put at risk.

D&O liability can stem from any type of operational risk including fraud risk as was the case with the Wirecard fraud. The above case studies underscore the importance of having robust D&O insurance coverage in place.,

Even the largest and most established organizations can face unexpected legal challenges that can threaten the personal finances of their key decision-makers. By investing in D&O coverage, companies can protect their directors and officers and financials, in turn allowing them to make strategic decisions.

D&O Insurance Dictionary

Cost of Officers and Directors Insurance

The cost of officers and directors insurance varies greatly depending on the nature of the organization being insured alongside the protection amounts and the type of coverage sought (ex. small D&O insurance limits can cost less than $1,000 for non-profit organizations whereas large limits for public companies can cost hundreds of thousands, or millions, of dollars).

Pleaser refer to the section above titled 'Cost of D&O Insurance Explained' for further details or use our D&O Insurance Cost Calculator for basic guidance.

D&O Insurance Policy

The D&O Insurance Policy is divided into several sections and incorporates the application signed by the insured as well as written correspondence confirming the insured's data on D&O risk, the declarations pages summarizing coverage, the main policy wording, and any endorsement that alters the main policy wording.

This follows more or less the same policy structure as any liability business insurance. Various insurers use a modular D&O insurance policy whereby the main policy wording is divided into sub wordings, each respecting a specific coverage that can be tagged onto the wording outlining general terms and conditions, which governs all sub wordings.

Directors Liability Insurance Cost

The cost of directors liability insurance can be lower than the overall D&O insurance cost which includes entity coverage simply by removing coverage afforded to the entity itself and focusing solely on coverage afforded to individual directors.

Directors and Officers Insurance for Non-Profit Organizations Cost

The cost of directors and officers insurance for non-profit organizations is much lower than the directors and officers insurance cost for private or publicly traded entities. This is due to the fact that the risk of monetary demands and lawsuits related to shares or securities is non existent in non-profit organizations, hence greatly reducing the directors and officers insurance risk to insurers.

Directors and Officers Liability Insurance

This is the same as directors and officers insurance or D&O insurance or D&O Liability Insurance. Various titles are used to describe the same product.

Please refer to the sections above for comprehensive content including the ability to instantly purchase directors and officers liability insurance.

Officers and Directors Insurance

It offers the same coverage as directors and officers insurance, which you can learn more about above.

D and O Insurance

A variant title describing D&O Insurance.

D & O Insurance

A variant title describing D&O Insurance.

D and O Insurance Quotes

These are summaries of pricing and coverage indications for a specific business.

SMEs or larger entities looking for D and O insurance quotes can contact us. We are independent of any D and O insurance broker or lobbyist and can contractually guarantee the lowest D and O Insurance Cost for similar protection.

Our team makes D and O insurance brokers compete to get you the best D and O insurance quote, as well as rewords and triggers the D and O insurance policy for best results.

We can also audit any D and O insurance quotes that Management has already sourced from brokers or insurers. Our AI-based independent insurance audit utilizes world leading commercial insurance analytics and minimizes D&O insurance cost.

Directors and Officers Insurance Quote

Please reference the above query.

Get a tailored Directors and Officers Insurance Quote instantly with an upfront fee of $500.

The lowest cost of such directors and officers insurance quote is contractually guaranteed (our firm forgoes any balance of fees due and subsidizes premium differences if you have legal proof of lower directors and officers insurance cost elsewhere for similar protection).

D&O Insurance Quote

Please reference the above query. Getting a quote for D&O insurance follows the same general principles as quotes for business insurance.

Directors and Officers Insurance for Nonprofits

See the section above called D&O Insurance for Nonprofits. Nonprofits have a unique D&O risk profile due to no share structure, which eliminates any risk of securities litigation to the insurers. This in turn leads to much lower directors and officers insurance for non-profit organizations cost.

D & O Insurance Not For Profit

See above as the term D & O insurance not for profit is simply a variant of Directors and Officers Insurance for Nonprofits or D&O Insurance for nonprofits.

Management Act

- This defines coverage under a D&O insurance policy through its insuring agreement, which is a policy clause outlining what is explicitly covered.

- Management Act is defined differently from one policy to the next. It is important to tailor the definition to the operational data of the business.

- Here is an example of a definition of Management Act within a D&O insurance policy:

"any actual or alleged defamation, breach of duty, neglect, error, misstatement, misrepresentation, omission or other act done or attempted by the INSURED PERSONS in the discharge of their duties solely in their capacity as INSURED PERSONS of the ENTITY or any matter claimed against them solely by reason of their status as INSURED PERSONS."

Semantic Variations of D&O Insurance

Semantic variations include the following depending on the country and content within which D&O insurance is used:

- Directors and Officers Insurance

- D&O liability insurance

- Directors insurance

- Directors Liability Insurance

- Director and Officer Liability Insurance

- dno insurance

- Management Liability Insurance

- Executive Liability Insurance

- Corporate Officer Insurance

- Board of Directors Insurance

- Directors Liability Coverage

- Officer Liability Coverage

- Directors & Officers Liability Insurance

- Management Indemnity Insurance

- Corporate Governance Insurance

Wrongful Act

- This defines comprehensive coverage under a D&O insurance policy and includes other defined terms such as Management Act, Employment Act, Fiduciary Act, or any Act that is defined under the policy.

- Wrongful Act reads differently from one policy to the next. It is important of such definition to be audited by an insurance consultant independent of brokers.