Insurance for security companies should generally be designed around the actual services performed, contractual obligations accepted, jurisdictions of operation, client types, workforce structure, vehicle use, technology systems, and potential severity of a major claim.

A generic business insurance package is not enough. The most important issue is not simply whether a security company has insurance. The more important question is:

Will the insurance program respond to the actual scenarios capable of causing the company its largest financial losses?

Review or Procure Insurance for Security Companies

👉 Independently of the broker placement process.

👉 The lowest premium is contractually guaranteed for similar protection tailored to your goals, otherwise we pay the difference. Applicable worldwide.

👉 Our broker-independent insurance engineers save clients 10–35% on insurance for security companies while eliminating coverage gaps that could cost far more later.

👉 Our team also provides Full Claims Management with Cash Advance at Loss, which is outside of the purview of brokers.

What Is Insurance for Security Companies?

Insurance for security companies is a combination of commercial insurance policies designed to protect businesses that provide security, guarding, patrol, monitoring, protective, investigative, access-control, surveillance, or related risk-management services.

Security companies operate in an unusual risk environment. Their employees may be expected to prevent theft, control access, protect property, respond to incidents, monitor surveillance systems, patrol client premises, manage crowds, document suspicious activity, or make rapid decisions when people and assets are at risk.

A security company can face allegations not only because an employee did something wrong, but also because a guard allegedly failed to act, failed to observe, failed to report, failed to respond, or failed to prevent a loss.

Depending on the operation, security company insurance may be relevant to:

- Security guard companies

- Private security companies

- Unarmed guarding businesses

- Mobile patrol companies

- Event security firms

- Concierge security providers

- Retail loss-prevention contractors

- Construction-site security companies

- Industrial security contractors

- Corporate security providers

- Alarm response companies

- CCTV monitoring businesses

- Executive protection firms

- Security consulting companies

- Investigation businesses

- Security technology providers

- Remote monitoring operations

- Government security contractors

- International security service providers

The appropriate insurance structure can vary substantially between these businesses.

A company providing reception-desk access control at office buildings does not have the same risk profile as a company providing mobile patrols, event security, high-value asset protection, or services in politically unstable regions.

Security companies may need a coordinated combination of the following products that must be reworded to be tailored to a company's operational risk:

- Commercial general liability insurance

- Security guard liability insurance

- Professional liability or errors and omissions insurance

- Workers’ compensation or employers’ liability

- Commercial auto insurance

- Cyber insurance

- Crime and fidelity coverage

- Property and equipment insurance

- Employment practices liability insurance

- Directors and officers liability insurance

- Umbrella or excess liability insurance

- Kidnap, ransom or crisis-response coverage for qualifying international exposures

- Specialized extensions for higher-risk security operations

Get an Independent Insurance Review

- Security companies can face substantial financial exposure from a single allegation involving negligence, failure to perform, employee conduct, vehicle operations, cyber incidents or contractual obligations.

- An independent insurance review can help determine whether the existing insurance program is aligned with the company’s actual operations.

- Review your security company insurance before the next major claim tests it.

👉 Start an Independent Insurance Audit

What Insurance Does a Security Company Need?

Most security companies should evaluate at least the following coverage categories:

**Important:** Coverage names alone do not determine protection. Definitions, exclusions, endorsements, sublimits, conditions, warranties and the interaction between policies can materially change the outcome of a claim.

Why Security Companies Have a Distinct Insurance Risk Profile

Security companies are different from ordinary service businesses because their core commercial purpose is often connected to the prevention, detection, deterrence, reporting or management of harmful events.

That creates a difficult liability dynamic.

If a theft occurs, a client may allege inadequate patrols.

If an unauthorized person enters a building, a client may allege access-control failure.

If an incident escalates, allegations may focus on employee conduct, training or supervision.

If a guard does not intervene, the company may face allegations of failure to act.

If surveillance footage is unavailable, the dispute may involve monitoring, retention, technology or contractual performance.

If an incident report is incomplete, documentation itself may become important to the defense of a claim.

This means the security company’s insurance program should be mapped to both:

1. **Affirmative acts** — what employees allegedly did; and

2. **Omissions** — what employees allegedly failed to do.

The Main Types of Insurance for Security Companies

1. Commercial General Liability Insurance

Commercial general liability insurance for security companies is usually a foundational component of the insurance program.

Depending on the wording and circumstances, it may respond to covered claims involving:

- Third-party bodily injury

- Third-party property damage

- Certain personal and advertising injury allegations

- Legal defense costs

- Certain incidents arising from business operations

Example

A visitor alleges that a security company’s operations contributed to an injury at a client location. The claim may trigger analysis under the company’s general liability policy.

However, the existence of a CGL insurance policy does not automatically mean every incident involving a guard is covered.

Security companies should examine:

- Who qualifies as an insured

- Scope of insured operations

- Description of business activities

- Assault-and-battery wording

- Expected or intended injury exclusions

- Professional services exclusions

- Abuse or molestation exclusions

- Contractual liability provisions

- Care, custody or control restrictions

- Employee injury exclusions

- Additional insured endorsements

- Deductible or self-insured retention structure

- Defense-cost treatment

- Territorial limitations

For security businesses, these provisions can be more important than the policy’s headline limit.

2. Security Guard Liability Insurance

Security guard liability insurance generally refers to liability protection designed for the specific operational exposures of guarding and security businesses.

Potential allegations may include:

- Negligent security

- Failure to patrol

- Failure to monitor

- Failure to respond

- Improper access control

- Inadequate incident escalation

- Negligent supervision

- Inadequate employee training

- Failure to follow post orders

- Failure to document an incident

- Alleged misconduct during security operations

The exact scope depends on the policy.

A major mistake is assuming that a policy marketed as “security guard insurance” necessarily covers every activity performed by the company.

The actual wording should be reviewed against the company’s:

- Contracts

- Website

- Proposals

- Invoices

- Employee roles

- Client industries

- Operating procedures

- Geographic footprint

- Subcontracted services

3. Professional Liability Insurance for Security Companies

Professional liability insurance —also called errors and omissions insurance or E&O insurance— may respond to covered allegations involving negligent professional services, mistakes, errors or failures to perform.

This can be particularly important where the company provides:

- Security consulting

- Risk assessments

- Security planning

- Threat assessments

- Site surveys

- Security-system recommendations

- Monitoring services

- Written security advice

- Emergency planning

- Corporate security consulting

- Security audits

Example

A security consultant recommends a particular access-control strategy. Following a major loss, the client alleges that the advice was negligent and caused financial damage.

A general liability policy may not be designed for pure financial loss arising from professional advice. Professional liability coverage may therefore be important.

4. Workers’ Compensation Insurance

Security companies are often labour intensive. Guards may work:

- Overnight shifts

- At construction sites

- In warehouses

- At retail premises

- At events

- In isolated locations

- Around members of the public

- In mobile patrol roles

- Under physically demanding conditions

Workers’ compensation requirements vary by jurisdiction, but coverage is commonly important and may be legally required where employees are present.

Key underwriting factors can include:

- Payroll

- Employee count

- Job classifications

- Claims history

- Work locations

- Shift patterns

- Nature of client sites

- Training procedures

- Use of subcontractors

5. Employers’ Liability Insurance

Employers’ liability insurance can address certain employee injury claims that fall outside or alongside the applicable statutory workers’ compensation framework, depending on jurisdiction and wording.

Security companies should pay particular attention to the interaction between:

- Workers’ compensation

- Employers’ liability

- General liability

- Contractual indemnities

- Subcontractor arrangements

6. Commercial Auto Insurance for Security Companies

A security company may need commercial auto insurance if it owns, leases or operates vehicles for:

- Mobile patrol

- Alarm response

- Supervisor visits

- Site inspections

- Employee transportation

- Equipment movement

- Client-service operations

The insurance review should consider:

- Owned vehicles

- Leased vehicles

- Hired vehicles

- Non-owned vehicles

- Employee-owned vehicles used for business

- After-hours vehicle use

- Driver screening

- Telematics

- Geographic radius

- Emergency-response expectations

A major gap can arise when employees use personal vehicles for company business without appropriate coordination between personal and commercial insurance arrangements.

7. Cyber Insurance for Security Companies

Cyber insurance is increasingly relevant because modern security businesses may hold or access:

- Surveillance footage

- Access-control records

- Visitor logs

- Employee records

- Incident reports

- Client building information

- Alarm data

- Patrol records

- GPS information

- Mobile-app data

- Cloud-hosted security information

- Credentials for client systems

Potential cyber events include:

- Ransomware

- Data breach

- Unauthorized access

- Business email compromise

- Privacy incidents

- System interruption

- Vendor compromise

- Credential theft

Security companies should also examine whether their cyber policy addresses the operational consequences of technology failure.

8. Crime and Fidelity Insurance

Crime insurance or a Fidelity Bond may be relevant because security employees can have trusted access to:

- Client premises

- Keys

- Restricted areas

- Inventory

- Sensitive information

- High-value property

Potential coverage categories can include:

- Employee dishonesty

- Forgery

- Certain theft events

- Computer fraud

- Funds-transfer fraud

The exact triggers and exclusions require careful review.

9. Employment Practices Liability Insurance

Security companies can employ large, distributed workforces with:

- Shift work

- Multiple supervisors

- High employee turnover

- Numerous client locations

- Decentralized management

- Promotion and scheduling decisions

Employment practices liability insurance may respond to covered allegations involving:

- Wrongful termination

- Discrimination

- Harassment

- Retaliation

- Certain employment-related misconduct

The policy should be coordinated with HR practices and jurisdiction-specific employment law.

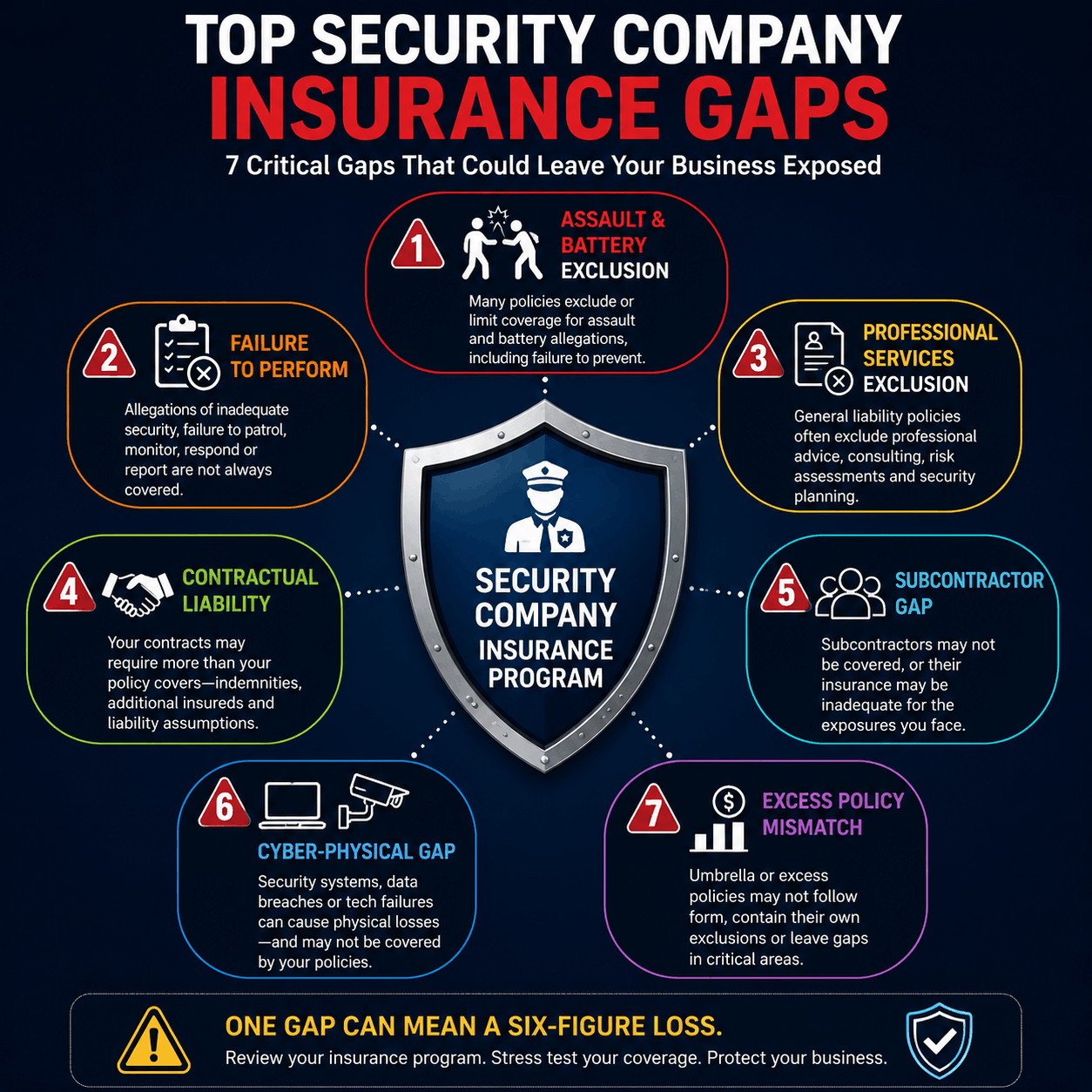

10. Umbrella and Excess Liability Insurance

A serious liability event can exceed the limits of an underlying policy.

Umbrella or excess liability insurance may provide additional limits above specified underlying policies.

Security companies should not assume that an excess policy automatically follows every aspect of the underlying coverage.

Review:

- Follow-form wording

- Scheduled underlying policies

- Exclusions

- Attachment points

- Defense costs

- Exhaustion requirements

- Sublimits

- Differences in conditions

11. Directors and Officers Insurance

Larger security companies, investor-backed firms and rapidly growing operators may consider **directors and officers insurance**, or D&O insurance.

Potential allegations can involve:

- Governance

- Misrepresentation

- Regulatory matters

- Investor disputes

- Management decisions

- Financial distress

- M&A transactions

D&O insurance protects a different risk category from security guard liability insurance.

Security Company Insurance Coverage Matrix

**Important:** This matrix is illustrative only. Actual coverage depends on policy wording, facts, jurisdiction, exclusions, conditions and endorsements.

The Biggest Insurance Gaps for Security Companies

1. Assault and Battery Exclusions

One of the most important issues in **security guard insurance** is assault-and-battery wording.

A policy may contain:

- A complete exclusion

- A partial exclusion

- A defense-only provision

- A sublimit

- A narrow carve-back

- Different treatment depending on who committed the act

For a security business, this can create a serious mismatch between operational risk and insurance protection.

### Questions to ask

- Is assault and battery excluded?

- Does the exclusion apply to alleged acts by employees?

- Does it also apply to failure-to-prevent allegations?

- Does it apply regardless of who caused the incident?

- Is negligent hiring or supervision also captured?

- Is there a separate sublimit?

2. Failure-to-Perform Exposures

Security companies are frequently retained to prevent or reduce loss.

A client may allege:

- Failure to detect intrusion

- Failure to respond

- Failure to call emergency services

- Failure to follow post orders

- Failure to monitor CCTV

- Failure to maintain staffing

- Failure to report suspicious activity

The key question is whether these allegations fall within covered professional services or are restricted elsewhere.

3. Professional Services Exclusions

A general liability policy may exclude professional services.

This becomes problematic if the company provides:

- Risk advice

- Site assessments

- Security planning

- Consulting

- System recommendations

A separate E&O policy may be needed, but the interface between CGL and E&O should be tested.

4. Contractual Liability Gaps

Security contracts may contain:

- Broad indemnities

- Defense obligations

- Additional insured requirements

- Waivers of subrogation

- High insurance limits

- Performance guarantees

- Liability for subcontractors

A company can contractually accept more liability than its insurance covers.

This is one of the most important reasons to review client contracts alongside insurance policies.

5. Subcontractor Gaps

Security companies may use subcontractors during:

- Large events

- Geographic expansion

- Seasonal demand

- Major client mobilizations

Key questions include:

- Are subcontractors covered?

- Are they required to carry their own insurance?

- Are certificates collected?

- Are limits adequate?

- Is indemnification in place?

- Does the policy restrict subcontracted work?

6. Armed vs. Unarmed Classification Errors

Insurers price and underwrite security companies based partly on actual activities.

If operations change during the policy term, the company should evaluate whether the insurer must be notified.

Material differences in exposure can affect:

- Eligibility

- Pricing

- Exclusions

- Required controls

- Claims analysis

7. Abuse or Molestation Exclusions

Security companies operating around:

- Schools

- Healthcare facilities

- Residential environments

- Vulnerable populations

should examine abuse and molestation wording carefully.

A broad exclusion may affect allegations beyond what management initially expects.

8. Cyber-Physical Coverage Gaps

Modern security companies increasingly combine personnel with technology.

Examples include:

- CCTV

- Access control

- Remote monitoring

- Mobile patrol applications

- Cloud dashboards

- Electronic incident reporting

A technology failure can create both:

1. A cyber event; and

2. A physical security loss.

The cyber and liability policies should be reviewed together.

Independent Insurance Engineering for Security Companies

Security businesses are paid to identify threats before they become losses.

Their insurance programs should be managed with the same discipline.

Independent insurance engineering can evaluate:

- Coverage gaps

- Policy exclusions

- Premium efficiency

- Limit adequacy

- Claims readiness

- Contractual risk

- Broker recommendations

- Insurer terms

- Financial exposure

The objective is not simply to buy more insurance.

The objective is to improve the relationship between: Risk → Policy Wording → Premium → Claim Trigger → Financial Recovery

How Much Does Security Company Insurance Cost?

The cost of insurance for a security company can vary substantially.

Pricing depends on factors such as:

- Country

- State or province

- Annual revenue

- Payroll

- Number of employees

- Number of guards

- Nature of services

- Client industries

- Contract size

- Claims history

- Coverage limits

- Deductibles

- Vehicle fleet

- Use of subcontractors

- Geographic scope

- International operations

- Risk controls

- Training programs

Published market estimates vary significantly, which is itself an important warning against relying on a single generic online average.

**Important:** These figures are broad planning illustrations, not quotations or guaranteed market averages. Actual premiums can fall below or above these ranges.

These ranges are illustrative only.

What Factors Affect Security Guard Insurance Cost?

1. Type of Security Services

A company’s actual services are among the most important underwriting variables.

Insurers may distinguish between:

- Static guarding

- Concierge security

- Mobile patrol

- Event security

- Retail security

- Industrial security

- Alarm response

- Security consulting

- International operations

2. Number of Employees

More employees generally increase exposure to:

- Workplace injuries

- Employment disputes

- Supervision failures

- Operational incidents

3. Payroll

Payroll can be a major rating variable for:

- Workers’ compensation

- Certain liability policies

4. Revenue

Higher revenue may indicate:

- More contracts

- Greater activity

- Larger clients

- Greater potential claim severity

5. Client Type

The same number of guards can generate very different risks depending on where they work.

6. Claims History

Prior claims can affect:

- Premium

- Deductible

- Coverage terms

- Market availability

- Underwriting scrutiny

7. Contractual Requirements

Large clients may require:

- Higher liability limits

- Additional insured status

- Specific endorsements

- Waivers

- Primary and non-contributory wording

Insurance for Different Types of Security Companies

Insurance for Unarmed Security Companies

Unarmed security companies may still face serious allegations involving:

- Negligent security

- Failure to intervene

- Failure to patrol

- Access-control errors

- Property loss

- Inadequate supervision

“Unarmed” does not mean “low liability.”

Insurance for Mobile Patrol Companies

Mobile patrol companies should consider:

- Commercial auto

- Hired and non-owned auto

- Driver screening

- Patrol radius

- Vehicle technology

- Employee vehicle use

Insurance for Event Security Companies

Event security firms can face:

- Crowd-related claims

- Access-control disputes

- Temporary workers

- Subcontractor exposure

- High concentrations of people

- Contractual indemnity requirements

Insurance for Retail Security and Loss Prevention Companies

Potential risks include:

- Wrongful detention allegations

- Bodily injury claims

- Property disputes

- Personal injury allegations

- Employee misconduct

- Failure to prevent theft

Policy wording should be examined against actual loss-prevention procedures.

Insurance for Construction-Site Security Companies

Construction-site security can involve:

- Theft

- Vandalism

- Fire

- Trespass

- Equipment loss

- Failure-to-patrol allegations

The security company should not assume it is insured for the full value of client property merely because it guards the site.

Insurance for Security Consulting Companies

Security consultants may have significant professional liability exposure because clients rely on:

- Recommendations

- Risk assessments

- Security plans

- Threat analyses

- Written reports

E&O insurance may be particularly important.

Security Company Insurance Requirements

There is no single worldwide insurance requirement for every security company.

Requirements can arise from:

1. National law

2. State or provincial law

3. Licensing regulations

4. Workers’ compensation statutes

5. Vehicle insurance laws

6. Client contracts

7. Landlord requirements

8. Government procurement rules

9. Industry certification

10. Lender or investor requirements

A security company should therefore evaluate both:

**Legally required insurance**

**Commercially required insurance**

These are not the same.

What Insurance Limits Should a Security Company Carry?

There is no universal answer.

A common starting point for some businesses may involve liability limits such as:

- $1 million per occurrence

- $2 million aggregate

However, larger clients or higher-severity operations may require:

- $5 million

- $10 million

- $25 million

- Higher limits

The correct limit should be based on:

- Maximum foreseeable loss

- Contract requirements

- Client concentration

- Jurisdiction

- Asset base

- Revenue

- Balance-sheet capacity

- Risk tolerance

The Security Company Insurance Limit Adequacy Test

A better method than copying a competitor’s insurance limit is to ask:

What is the plausible financial severity of our largest uninsured or underinsured event?

Consider:

- Maximum people concentration

- Largest client

- Highest-value site

- Largest contractual indemnity

- Largest vehicle accumulation

- Largest data exposure

- Largest employment exposure

- Largest international exposure

Then compare those values against:

- Policy limits

- Sublimits

- Deductibles

- Retentions

- Exclusions

How to Compare Security Company Insurance Quotes

- Do not compare quotes based only on premium. Use a structured comparison.

- A cheaper quote can be financially inferior if it removes coverage for the company’s most likely severe-loss scenarios.

Security Company Insurance Audit Checklist

Before renewing insurance, review:

### Operations

☐ All services disclosed

☐ New services disclosed

☐ Client industries reviewed

☐ Geographic changes reviewed

☐ Subcontractors reviewed

### Liability

☐ Assault and battery wording reviewed

☐ Professional services exclusion reviewed

☐ Contractual liability reviewed

☐ Additional insured obligations reviewed

☐ Failure-to-perform exposure reviewed

### Workforce

☐ Employee count accurate

☐ Payroll accurate

☐ Classifications accurate

☐ Training documented

☐ Claims reviewed

### Vehicles

☐ Fleet schedule accurate

☐ Drivers screened

☐ Hired auto reviewed

☐ Non-owned auto reviewed

### Technology

☐ Cyber exposure reviewed

☐ CCTV data considered

☐ Client system access reviewed

☐ Incident response plan tested

### Financial

☐ Limits stress-tested

☐ Deductibles affordable

☐ Excess layers reviewed

☐ Major uninsured scenarios quantified

How to Reduce Security Company Insurance Costs

Reducing insurance cost should not mean simply removing coverage.

Potential strategies include:

## 1. Improve Submission Quality

Provide insurers with:

- Clear service descriptions

- Claims analysis

- Training records

- Risk controls

- Client mix

- Contract procedures

- Driver controls

## 2. Correct Misclassification

Ensure the insurer accurately understands:

- Services

- Payroll

- Revenue

- Client types

- Geographic scope

## 3. Analyze Claims

Identify recurring patterns by:

- Location

- Employee

- Client

- Incident type

- Time of day

## 4. Review Deductibles

A higher deductible may reduce premium but increases retained risk.

The optimal deductible should reflect:

- Cash flow

- Claims frequency

- Balance sheet

- Risk tolerance

## 5. Review Contracts

Poor contractual terms can increase liability even when operations are well managed.

## 6. Use Independent Insurance Engineering

An independent review can analyze whether:

- Policies match operations

- Exclusions create gaps

- Limits are adequate

- Coverage overlaps

- Premium is efficient

- Claims procedures are aligned with policy conditions

Why Security Companies Should Review Insurance Before a Major Loss

Insurance disputes often become more difficult after a loss has already occurred.

Before a major claim, a company may be able to:

- Identify exclusions

- Negotiate endorsements

- Correct classifications

- Increase limits

- Improve documentation

- Align contracts

- Address policy overlaps

After the loss, those options may no longer be available for that event.

The best time to test an insurance program is generally before the company needs it.

Frequently Asked Questions

Disclaimer

This article provides general educational information only and does not constitute legal advice, insurance advice, a quotation, a guarantee of coverage or a recommendation to purchase any specific policy. Insurance availability, terminology, requirements, exclusions and pricing vary by insurer, jurisdiction, policy wording and individual risk. Actual policies and contracts should be reviewed by qualified professionals.