Course of Construction Insurance is specialized property insurance designed to protect buildings, structures, construction work, materials and other insured property while a project is being built, renovated or redeveloped. It is commonly called COC insurance or Builder’s Risk Insurance, although exact coverage depends on the policy wording, exclusions, limits and jurisdiction.

Is Your Course of Construction Insurance Designed to Pay?

A policy can exist while major gaps remain in existing structures, water damage, defective work, testing, soft costs, occupancy or project delay.

👉 Review or procure your construction insurance independently of the broker placement process.

👉 The lowest premium is contractually guaranteed for similar protection tailored to your goals, otherwise we pay the difference. Applicable worldwide.

👉 Our broker-independent insurance engineers save clients 10–35% on course of construction insurance while eliminating coverage gaps that could cost far more later.

Our team also provides Full Claims Management with Cash Advance at Loss, which is outside of the purview of brokers.

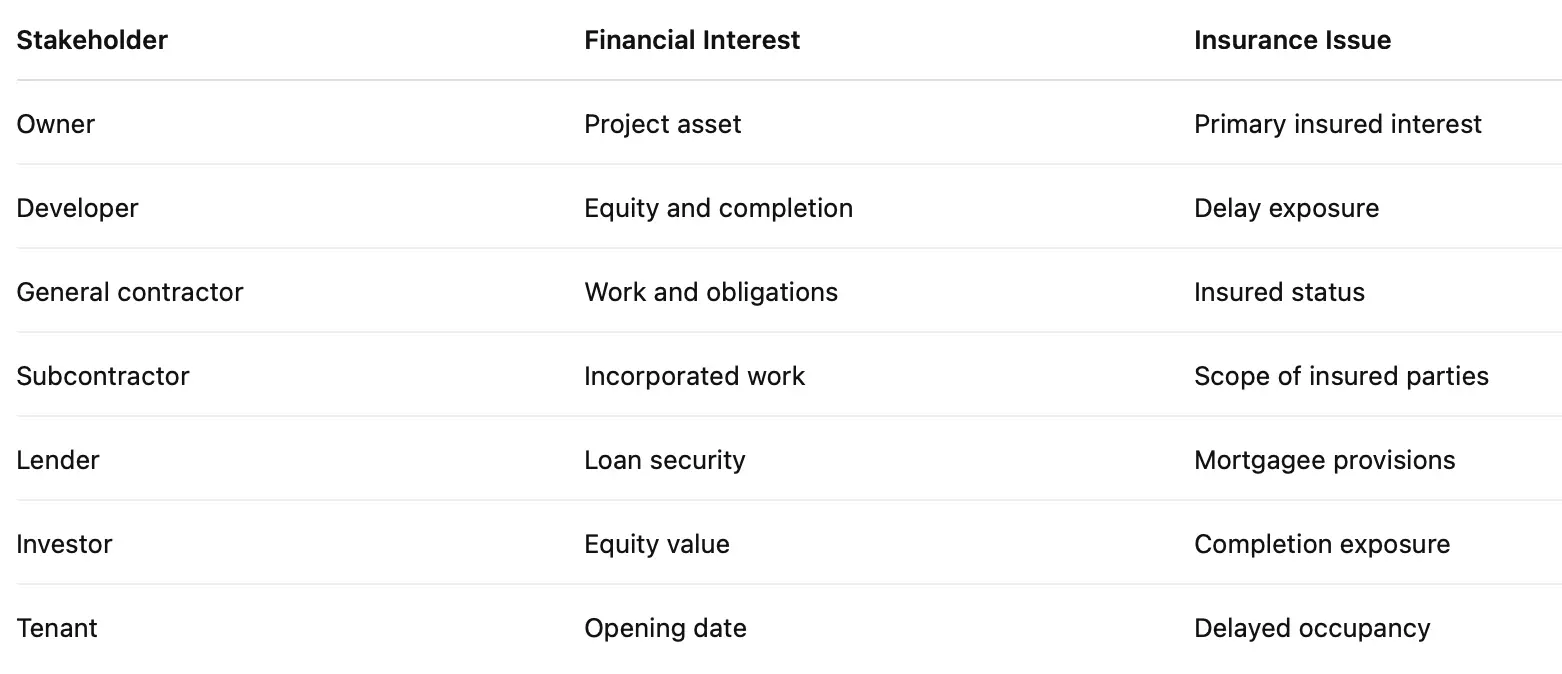

Course of Construction Insurance can be relevant to property owners, developers, contractors, lenders and investors because an active construction project creates risks that may not be adequately addressed by standard property insurance.

Depending on the policy, COC insurance may cover insured physical loss or damage involving:

- buildings under construction;

- construction materials;

- fixtures;

- equipment intended for permanent installation;

- temporary works;

- materials stored off-site;

- materials in transit;

- existing structures during renovations;

- debris removal;

- professional fees;

- specified soft costs; and

- certain financial losses caused by delayed completion after insured physical damage.

However, holding a Course of Construction Insurance policy does not mean every construction loss will be paid. Learn more about all risks insurance.

Coverage can be materially affected by exclusions involving defective design, faulty workmanship, water damage, flood, earthquake, testing, existing structures, occupancy, project delays, valuation and policy termination.

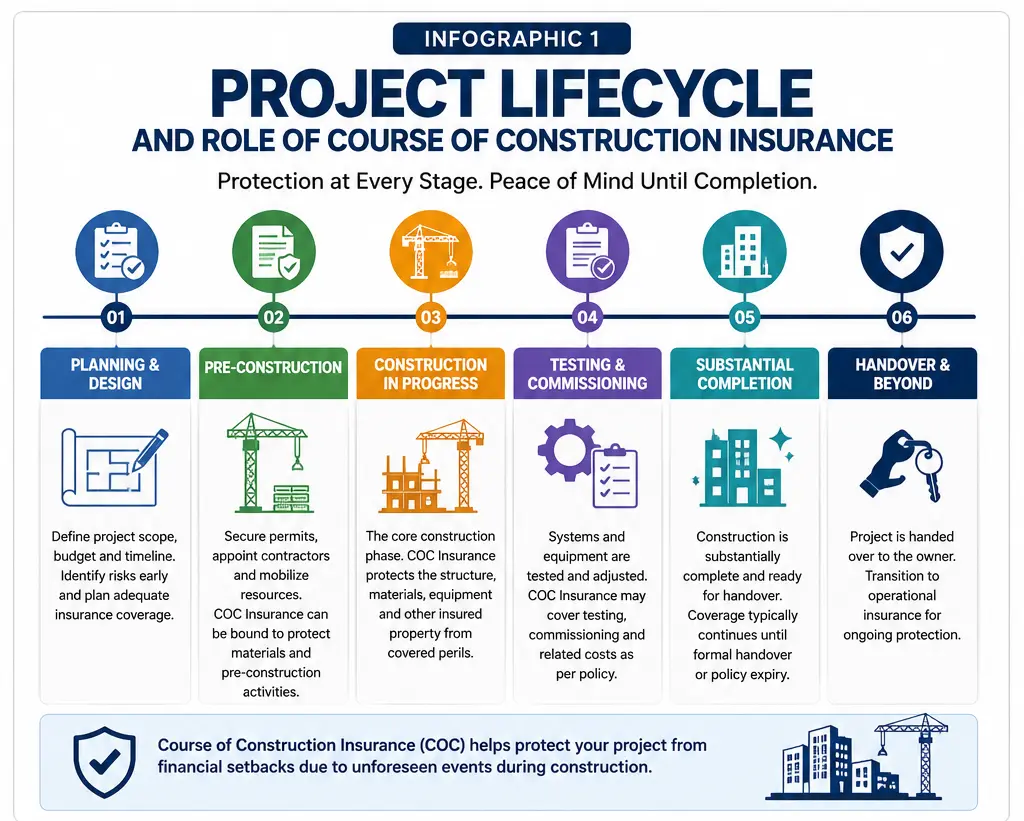

What Is Course of Construction Insurance?

Course of Construction Insurance protects insured property during the period when a building or project is being constructed, renovated, expanded or redeveloped.

A completed-building property policy may not adequately respond to the changing exposures created by active construction. During construction:

- project values continuously change;

- materials move between suppliers, storage locations and the project site;

- contractors and subcontractors perform interconnected work;

- temporary structures may be used;

- mechanical and electrical systems are tested;

- parts of the building may become occupied before final completion; and

- a major physical loss can delay revenue generation or increase financing costs.

COC insurance is designed for this transitional period.

The insured project may be:

- a residential development;

- commercial building;

- office tower;

- hotel;

- industrial facility;

- warehouse;

- infrastructure asset;

- institutional building;

- mixed-use development; or

- major renovation.

How Course of Construction Insurance Works

Is Course of Construction Insurance the Same as Builder’s Risk Insurance?

Usually, yes. Course of Construction Insurance and Builder’s Risk Insurance commonly describe the same general category of construction-phase property insurance. However, the terms should not automatically be treated as proof of identical coverage.

Two policies with similar names can differ materially in their treatment of:

- existing structures;

- flood;

- earthquake;

- water damage;

- defective workmanship;

- testing and commissioning;

- off-site materials;

- materials in transit;

- soft costs;

- delayed opening;

- partial occupancy; and

- policy termination.

Key takeaway: Compare the actual insuring agreement, definitions, exclusions, limits, sublimits, deductibles and endorsements—not merely the policy name.

What Does Course of Construction Insurance Cover?

Coverage depends on the insurer, policy wording, project and endorsements.

A Course of Construction policy may insure direct physical loss or damage to specified project property from covered causes of loss.

Commonly Insured Property

What Events Can COC Insurance Cover?

Depending on the wording, COC insurance may cover insured physical loss or damage caused by events such as:

- fire;

- lightning;

- explosion;

- theft;

- vandalism;

- windstorm;

- hail; and

- other accidental causes of loss not otherwise excluded.

Coverage for flood, earthquake, named windstorm, water damage, collapse, testing, pollution and other specialized exposures may be excluded, restricted, sublimited or separately endorsed.

What Does Course of Construction Insurance Not Cover?

Common exclusions or restrictions may involve:

- defective design;

- faulty workmanship;

- defective materials;

- wear and tear;

- corrosion;

- gradual deterioration;

- mechanical breakdown;

- electrical breakdown;

- pollution;

- war;

- nuclear risks;

- intentional acts; and

- other policy-specific exclusions.

Third-party bodily injury and third-party property damage are generally different exposures from first-party damage to the construction project. Separate liability insurance may therefore be required.

Workers’ injuries, automobiles, contractors’ mobile equipment, professional design liability and cyber risks may also require separate insurance arrangements.

Course of Construction Insurance for Renovations

Renovation projects create a particularly important issue: the existing structure.

Consider a building worth $10 million undergoing a $3 million renovation.

If the COC policy covers only the $3 million of new work, while the existing property policy restricts coverage because major construction is underway, a fire affecting both old and new portions could create a substantial insurance gap.

For renovation projects, decision-makers should determine:

Is the existing structure insured, by which policy, for what value and subject to what construction-related restrictions?

This issue can affect:

- office conversions;

- hotel renovations;

- residential additions;

- industrial retrofits;

- heritage buildings;

- shopping centres; and

- adaptive-reuse projects.

Learn more about the types of assets that can be covered under commercial property insurance.

Course of Construction Insurance and Soft Costs

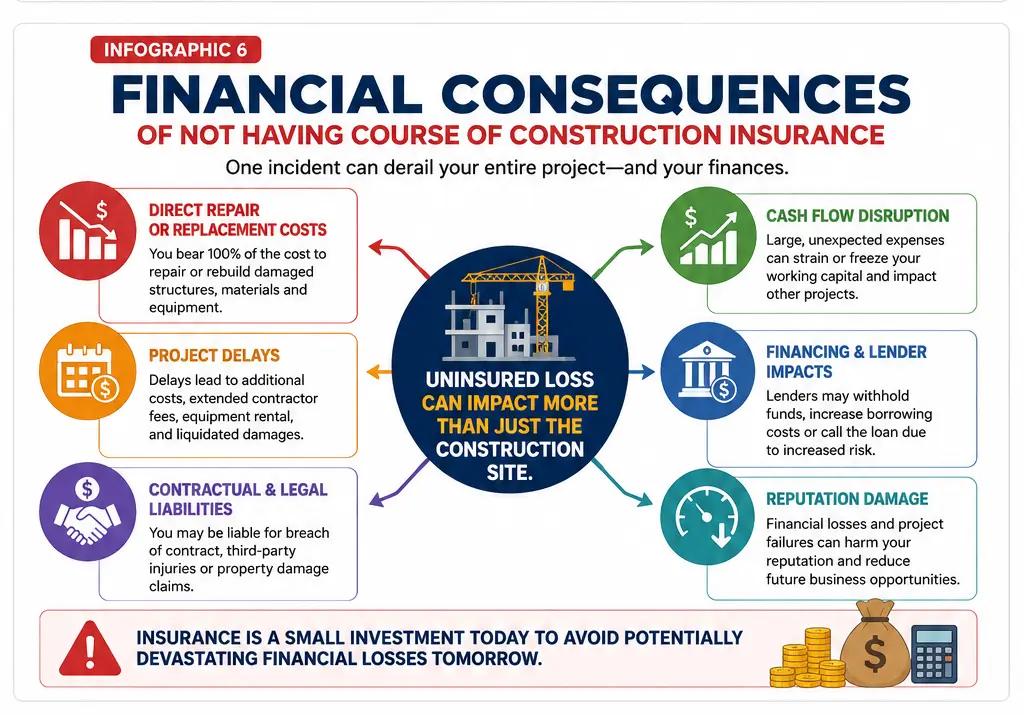

A physical loss can create financial costs far beyond repairing damaged property.

Suppose a fire causes direct physical damage and delays project completion by nine months. The developer may also face:

- additional loan interest;

- extended professional fees;

- additional real estate taxes;

- permit-related expenses;

- additional insurance expense;

- extended project administration; and

- other specified carrying costs.

These exposures are often described as soft costs.

Soft-cost coverage should not be confused with a general guarantee against project delay. Coverage commonly depends on delay resulting from insured physical loss or damage.

A policy can respond well to direct physical damage while responding poorly to the resulting financial delay.

What Is Delay in Start-Up or Delayed Opening Insurance?

Large commercial, industrial and infrastructure projects may require coverage for financial loss caused by delayed completion following insured physical damage.

Terminology can include:

- Delay in Start-Up or DSU;

- Advanced Loss of Profits or ALOP; and

- Delayed Opening coverage.

For example, if insured physical damage delays the opening of a hotel, factory, apartment development or logistics facility, the project may lose expected revenue while continuing to incur financing costs.

Important variables can include:

- coverage trigger;

- indemnity period;

- waiting period;

- insured financial measure;

- projected revenue assumptions;

- saved expenses;

- project schedule;

- critical path; and

- concurrent delays.

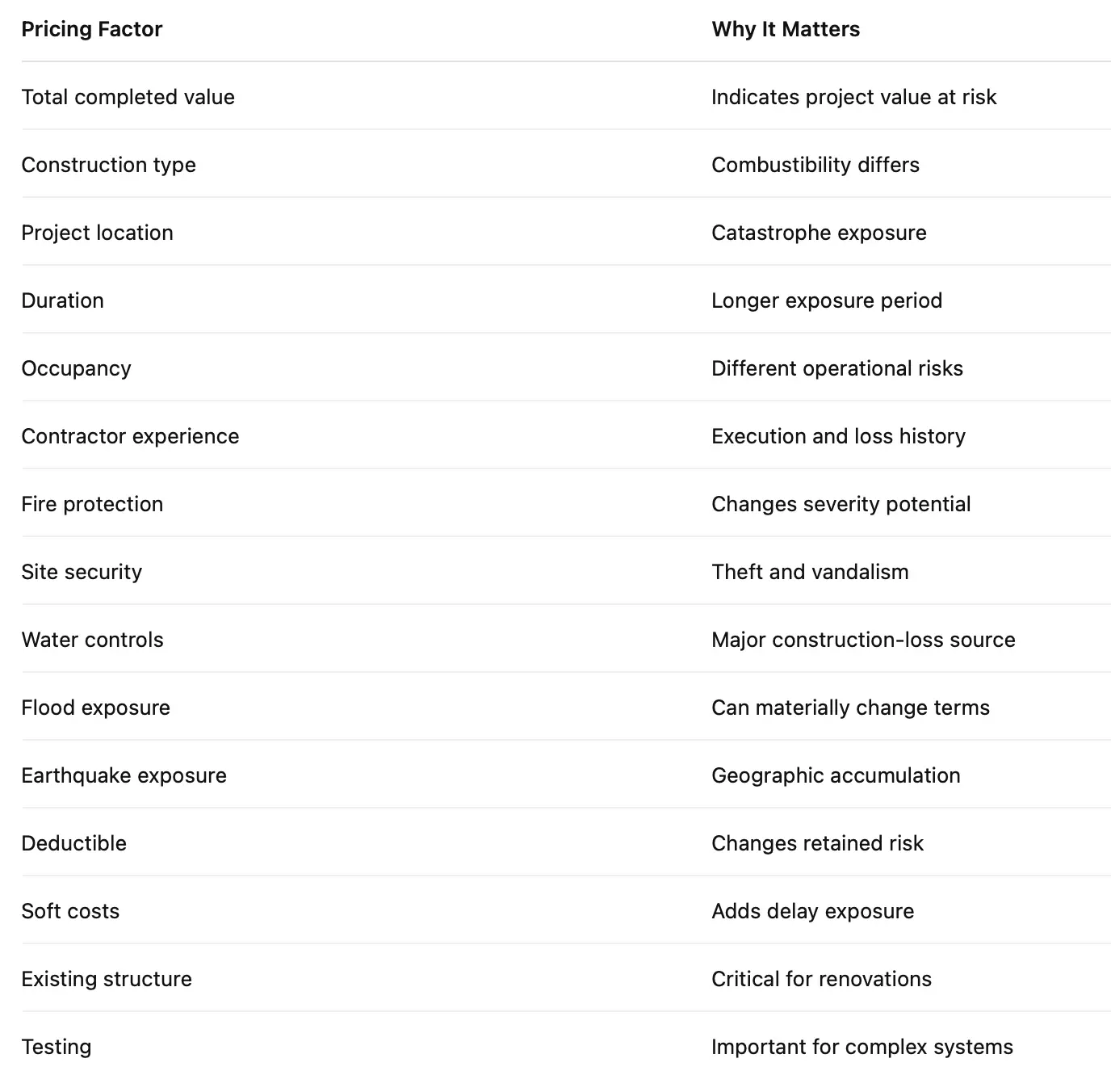

How Much Does Course of Construction Insurance Cost?

There is no universal Course of Construction Insurance price. Premium depends on project value, construction type, location, duration, catastrophe exposure, contractor experience, deductibles, selected coverage and other underwriting factors. Use our builders risk insurance cost calculator for instant premium estimates.

Illustrative Cost Formula

Estimated COC Premium = Project Value × Indicative Rate × Risk Adjustments

Risk adjustments may reflect:

- construction type;

- project duration;

- location;

- catastrophe exposure;

- deductibles;

- loss history;

- fire protection;

- water controls;

- security;

- testing; and

- delay coverage.

For project-specific benchmarking, use DeshCap’s Builders Risk Insurance Cost Calculator.

Who Should Buy Course of Construction Insurance?

The party responsible for arranging COC insurance should be determined by:

- the construction contract;

- financing documents;

- ownership structure; and

- allocation of project risk.

Depending on the project, the policyholder may be:

- owner;

- developer;

- general contractor;

- construction manager; or

- another party with an insurable interest.

Other stakeholders may need protection as named insureds, additional insureds, loss payees, mortgagees or lenders, depending on the policy and their legal interest.

Who Should Be Named on a Course of Construction Policy?

Potential stakeholders can include:

- project owner;

- developer;

- general contractor;

- construction manager;

- subcontractors;

- lenders; and

- other parties with an insurable interest.

Course of Construction Insurance for Lenders and Investors

Construction insurance is not only an insurance procurement issue. It can affect financing, liquidity and valuation.

Lenders may require:

- specified coverage;

- minimum limits;

- insured status;

- notice provisions; and

- evidence of insurance.

Investors may care about whether a major loss creates:

- additional equity requirements;

- debt-service pressure;

- completion delays;

- covenant pressure; or

- valuation impairment.