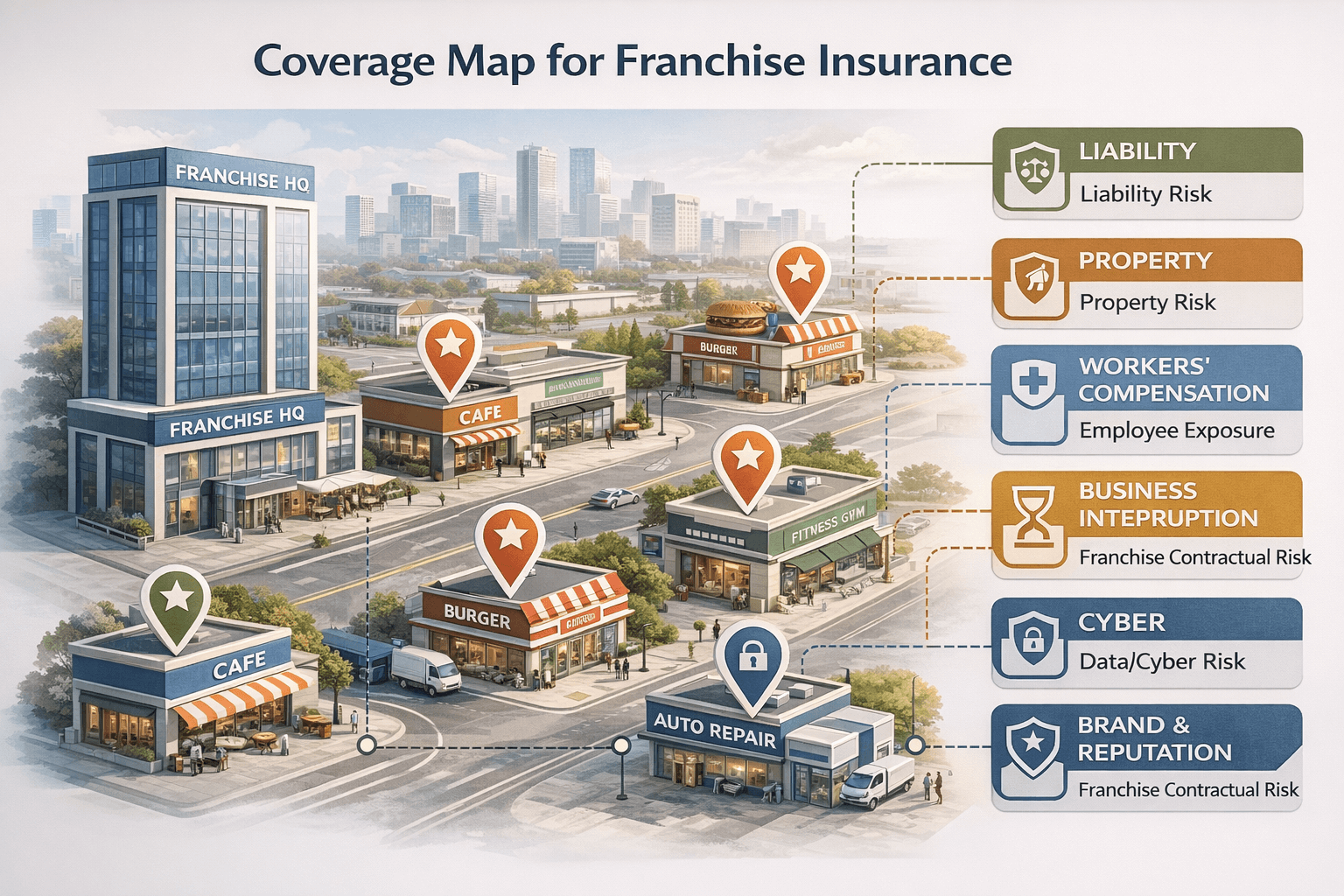

Franchise insurance protects both franchisors and franchisees from liability, property damage, employee injury, cyber exposure, and contractual risks unique to franchise systems operating across multiple locations and jurisdictions.

Get Franchise Insurance

The lowest premium is contractually guaranteed for similar protection tailored to your goals, otherwise we pay the difference. Applicable worldwide.

👉 Our independent insurance engineers typically save clients 10–35% on franchise insurance while eliminating coverage gaps that could cost far more later. Our team also provides Full Claims Management with Cash Advance at Loss, which is outside of the purview of brokers.

Contact DeshCap today.

Franchise Insurance: A Comprehensive Overview

Franchise insurance is a suite of tailored insurance products designed to protect both franchisors and franchisees from financial loss due to operational risks such as fraud risks, liability, property damage, employee injuries, and contractual exposures unique to franchise systems.

Because franchise operations involve interdependent relationships between brand owners and individual franchise operators, franchise insurance must address:

- liability arising from customer incidents

- property damage at multiple locations

- employer liability across jurisdictions

- contractual obligations under franchise agreements

- intellectual property risk exposure

- product liability for franchised goods/services

Franchise insurance differs from standard commercial coverage in its need to align coverage with the structure and governance of the franchise network.

Our engineers can negotiate with franchise insurance brokers and manage claims, or provide Management with audits or analytics for their own execution.

DeshCap is ranked online #1 for Liability Risk worldwide and Top Operational Risk Advisor.

Essential Insurance for Franchises

Below are core coverages that franchise systems commonly require to safeguard against financial losses and ensure compliance with franchise agreements:

Franchise Liability Insurance

- Protects against third-party claims for bodily injury and property damage arising from franchise operations.

- Common scenarios include customer slips, service failures, or product defects.

- Liability limits are often designed to align with the franchise agreement.

Learn about Franchisor liability insurance.

Franchise Property Insurance

Protects physical assets at franchised locations, including buildings, equipment, inventory, signage, and fixtures used to generate revenue.

It can also be extended to include coverage for business interruption.

Workers’ Compensation for Franchise Systems

Because franchise businesses employ staff across multiple locations, workers’ compensation protects employees from occupational injuries, illness, and wage loss exposure.

Franchise Auto Insurance

Protects vehicles used in franchise operations, including delivery vans, service vehicles, and company-owned fleets.

Coverage typically includes bodily injury liability, property damage liability, physical damage to vehicles (collision and comprehensive), and uninsured/underinsured motorist protection.

Franchise auto insurance is particularly relevant for:

- Food delivery franchises

- Courier and logistics franchises

- Mobile service providers

- Field-based maintenance businesses

- Multi-location operators with shared fleet vehicles

Premiums are influenced by:

- Number and type of vehicles

- Driver records and MVR history

- Radius of operations

- Claims experience

- Use type (delivery vs service vs passenger transport)

Franchise agreements often require minimum commercial auto liability limits and may mandate additional insured endorsements to protect the franchisor.

For multi-unit franchise operators, structuring fleet insurance under a master commercial auto policy can improve cost efficiency while ensuring consistent liability protection across locations.

Franchise-Specific Risks

Franchises often need customized coverage to address:

- contractual reimbursements to franchisor

- breach of franchise agreement exposures

- brand reputation risk

- multi-state operations

- cyber & data breaches across locations

Insurance for franchises should at a minimum help cover legal costs, property damage, and employee-related claims, ensuring that the franchise operates smoothly and is protected from unforeseen events.

The policies should be tailored to specific industries and franchise operations, helping protect against risks such as product liability.

It is therefore important that the policies be structured to reflect the unique operational risks of the franchise or else their insurance payout ratios drop significantly.

How Franchise Insurance Cost Is Determined

Franchise insurance cost varies based on:

- number of locations

- total payroll

- type of industry (food vs retail vs services)

- loss history

- liability limits selected

- geographic risk factors

Franchise Insurance Risk Management & Audit

Franchise risk management audits assess:

- controls at franchised locations

- consistency of safety practices

- contractual insurance requirements

- franchise agreement indemnity language

- third-party vendor exposures

This helps reduce premium and strengthens compliance.

Learn more about what a risk audit entails.

Tailoring Franchise Business Insurance to Relevant Risks

Franchise business insurance is a crucial safeguard for both franchisors and franchisees, offering protection from a wide range of risks associated with running a franchise. Learn about the latest trends and operational matters impacting franchises through the likes of the International Franchise Association (IFA).

This type of insurance typically includes coverage for general liability, property damage, and business interruption, ensuring that the business can continue operating even after an unexpected event.

Investing in comprehensive franchise business insurance is essential for maintaining operational stability and protecting long-term investments.

Franchise Insurance Examples by Industry

Insurance requirements vary significantly across franchise industries. Major international franchise systems typically require franchisees to carry structured insurance programs aligned with contractual indemnity, brand protection, and operational risk exposure.

Below are examples by industry category.

Franchise Restaurant Insurance including QSRs

Major global food franchises such as McDonald’s, Subway, and KFC operate high-volume, customer-facing environments where liability exposure is elevated.

Franchise restaurant insurance for food brands typically emphasizes:

- General liability for customer injury (slip, fall, food contamination)

- Product liability coverage

- Property insurance for equipment and fixtures

- Business interruption tied to kitchen or fire damage

- Workers’ compensation for staff

- Umbrella liability limits aligned with franchise agreement requirements

Food franchise systems often require franchisees to list the franchisor as an additional insured and comply with minimum limit thresholds to protect the brand.

👉 Contact us to procure franchise restaurant insurance.

"DeshCap structured better products giving us better coverage at prices better than we had been previously paying" - Anthony Di Ioia, CFO of BeaverTails Canada Inc., a national Canadian franchisor of Food Pastries. Read full testimonial.

Coffee & Retail Café Franchise Insurance

International café brands such as Tim Hortons, Starbucks (licensed model in certain regions), and Costa Coffee typically require insurance programs tailored to:

- High daily customer traffic

- Hot beverage burn exposure

- Inventory and refrigeration loss

- Multi-location business interruption

- Cyber risk (POS systems and loyalty programs

Because café franchises rely heavily on brand reputation and operational consistency, property and liability wording must align with franchise contractual standards.

Retail & Consumer Product Franchise Insurance

Retail-focused franchise systems such as The UPS Store, 7-Eleven, and Ace Hardware require franchise insurance programs that address:

- Premises liability

- Inventory and stock coverage

- Theft and crime insurance

- Commercial auto exposure (if delivery or fleet involved)

- Cyber insurance for customer data and payment systems

Multi-unit retail franchise operators often structure umbrella and excess liability coverage across locations to manage aggregate exposure.

Fitness & Service Franchise Insurance

Service-based franchises such as Anytime Fitness, Orangetheory Fitness, and The UPS Store (service model) typically require:

- Professional liability (where services are advisory or physical)

- Participant injury liability

- Equipment breakdown coverage

- Employment practices liability (EPLI)

- Workers’ compensation

Fitness franchises, in particular, may face elevated bodily injury exposure, making liability limits and waiver alignment critical.

Automotive & Repair Franchise Insurance

Automotive franchise systems such as Midas, Jiffy Lube, and Meineke typically require:

- Garage liability insurance

- Garagekeepers legal liability

- Environmental impairment liability

- Commercial auto coverage

- Workers’ compensation

Because repair operations involve customer vehicles and mechanical service risk, policy wording around care, custody, and control is especially important.

Brand names referenced above are used for educational illustration of franchise insurance structures and do not imply affiliation or endorsement.

Important Note on Franchise Brand Insurance

Each franchise brand sets its own insurance requirements through its franchise agreement. These often include:

- Minimum liability limits

- Additional insured provisions

- Waiver of subrogation clauses

- Notice of cancellation endorsements

- Umbrella policy thresholds

Franchise insurance must be structured to satisfy these contractual requirements while also protecting the franchisee’s operational exposure.

Independent review of franchise insurance wording ensures that coverage aligns not only with brand requirements but also with real-world risk scenarios.

👉 Learn about our broker-independent business insurance review.

Franchisor Insurance: Types, Coverage, Updates

Aka. franchisor business insurance, it consists of various types of commercial insurance that are specifically designed to protect a franchisor from different forms of Operational Risk.

Franchisor Insurance includes but is not limited to the following:

· Directors’ & Officers’ Liability Insurance (D&O)

· Professional Liability Insurance (E&O)

· Commercial General Liability Insurance (CGL)

· Commercial Property Insurance

· Credit Insurance

· Other types of insurance depending on the nature of the franchisor

If you are a franchisor carrying one or more of the above-mentioned types of insurance, feel free to request a proposal from our team for quotes on analytics or management of your insurance independently of any broker or insurer (it's a quick 1 step process).

Our team has deep experience with franchisor insurance including the structuring of franchisee insurance programs from scratch.

Franchisor Insurance Market Updates

Due to the general hardening of the commercial insurance market around the world since Covid, premiums for Franchisor Insurance have been on an upward trend.

While this underwriting cycle typically lasts up to 7 years, franchisors can now access better premium and coverage in options.

Note that insurers shun franchise businesses using a broad brush approach, which does not differentiate between a franchise business that has a relatively low risk profile versus one that has a relatively high risk profile.

It is important to do an insurance broker rfp in order to hire the right national franchise insurance brokers at the right terms for your franchise.

More on Franchisor Insurance Coverage

The coverage provided by franchisor insurance largely depends on how it has been reworded to match the operational data of the franchisor.

For instance, if the franchisor bought insurance directly from a broker or insurer, the policy wording would not be tailored accordingly, as a result coverage would be limited to standard terms and conditions that the insurer had initially drafted.

This is dangerous for the franchisor because such insurance would have a low payout ratio (< 25% on average), would not be relevant to the franchisor’s operations, and would be more costly in terms of direct premiums paid as well as the cost of risk that was not eliminated due to the poor protection offered by such franchisor insurance.

A risk expert independent of brokers and insurers must be involved in rewording and clinically triggering the insurance policy for effective results.

In addition, it is important to keep updated with market dynamics impacting franchisor insurance coverage. For larger franchisors, it is recommended that their insurance coverage be reviewed and updated on a quarterly basis.

Linking Franchisor Insurance to Risk Management

- Each type of franchisor has its own unique operations and corresponding data, it is therefore important for risk management and insurance to be tailored accordingly.

- It is highly recommended to centralize the risk management and franchisor insurance as it relates to larger franchisors with operations in multiple jurisdictions.

- You can refer to our case study for a preview of some of our work on a franchisor client of ours within the food & beverage industry.

Franchisor Liability Insurance

This is one of the most important types of franchisor insurance simply due to the fact that the franchisor faces Liability Risk from several parties including its own franchisees, customers, as well as third parties such as landlords or service providers.

Depending on the jurisdiction in which the franchisor operates, they may be subject to franchisee rescission claims, which must be covered by the franchisor liability insurance.

Moreover, the insurance must be analyzed carefully, word by word, by risk experts independent of brokers and insurers.

👉 Contact us if you are looking to procure franchisor liability insurance.

Franchisor Directors & Officers (D&O) Insurance

- Liability from shareholders and other parties arising from the mismanagement of a franchisor should be covered by Franchisor D&O Insurance.

- The wording of the franchisor D&O insurance policy should be structured based on the specific quantum and types of D&O liability risks facing the franchisor.

Franchisor Errors & Omissions Insurance

- Aka. Franchisor E&O Insurance, it is a subset of franchisor liability insurance. It covers the franchisor due to liability as a result of the provision of its services.

- Service are generally provided to customers and franchisees however each franchisor is different in the type and breadth of services it offers.

Franchisor Professional Indemnity Insurance

- This is the same as Franchisor E&O Insurance, it’s just named differently.

- Please see the section above for more information or learn more about professional indemnity insurance.

Franchisor Cyber Liability Insurance

- Important when the franchisor is subject to relevant contractual obligations, customer data storage, and disruptions due to viruses or cyber attacks.

- This coverage is a main component of Franchise Cyber Insurance, which also provides first party non-liability coverage.

Franchisor Commercial General Liability Insurance

- General liability that is not covered by specialty franchisor liability insurance, such as slips and falls or advertising injury, should be covered by CGL insurance.

- This insurance is fairly standardized yet it is still important to audit its wording in relation to the general franchisor liability risks that matter the most.

- This can also include franchisor product liability insurance coverage in case of liability arising from the use or consumption of the franchisor's products.

Franchisee Insurance: An Overview

Most of the time, a franchisee is required by the franchisor to purchase specific types of commercial insurance. This insurance requirement should be included within the Franchise Agreement.

The requirement is different from one franchisor to another depending on industry and nature of operations. It is important for the franchisee to fully comply with the franchisor insurance requirements, which entail technical insurance obligations that cannot be met through the simple purchase of insurance directly from brokers and insurers.

A risk expert independent of brokers/insurers must be involved in the procurement and management process of the franchisee insurance.

Depending on the size and sophistication of the franchise, a franchisee may be subject to participation within a franchisor insurance sponsored program that offers standard terms and conditions across all franchisees.

👉 Contact us to procure franchisee insurance.

Franchisees Property Insurance

- Franchisees property insurance is an essential coverage for protecting the physical assets of a franchise, including buildings, equipment, and inventory.

- This insurance shields franchisees from financial loss due to events like fire, theft, vandalism, or natural disasters.

- Property insurance ensures that if any damage occurs to the franchise location or its contents, repairs or replacements are covered, minimizing business downtime.

Having comprehensive franchisees property insurance is a key component of risk management, allowing franchise owners to focus on running their business without the fear of unexpected property-related expenses.

Franchisees property insurance also has important implications for compliance with franchise agreements and landlord agreements.

Many franchise agreements require franchisees to maintain adequate property insurance to cover potential risks, ensuring the brand is protected from financial loss due to damage.

Additionally, landlord agreements for leased commercial spaces often mandate that tenants carry property insurance to protect the premises.

Failure to secure adequate franchisees property insurance could lead to violations of these agreements, resulting in penalties or termination of leases or franchise contracts.

Proper insurance ensures franchisees remain compliant, protecting both the business and its relationships with franchisors and landlords.

Franchise Insurance Programs Explained

It is highly recommended for a franchise to create an insurance program for its franchisees as it would provide standard terms and conditions, in addition to cost savings, to the franchisees.

In addition, a standardized way of protecting franchisees offers greater protection to the franchisor from a credit risk standpoint (ie. the franchisor’s revenue stream consisting of franchise fees, royalties, product revenue, etc., would be more secure when the franchisees’ operations are better protected against various types of Operational Risk).

Franchise insurance programs should be structured carefully with the right broker and insurer partners along with a framework that is tailored to the nature of the franchise.

Franchise Insurance Requirements

It is important for the insurance requirements within a Franchise Agreement to be clear and reasonable for the franchisees.

Many times, franchisees seek the help of the franchisor in leasing physical properties for which there are landlord insurance requirements, which must also be contemplated when drafting franchise insurance requirements.

The insurance requirements within the FA as well as corresponding material should be updated at least once a year to reflect changing operational trends and insurance market dynamics.

Franchise Risk Solutions

Risk solutions to franchises should be divided into 2 categories:

(1) Risk assessment and management, which includes the measurement of different types of franchise risks (ex. probability of occurrence and currency impact of cyber risk). This also includes any recommendations and corresponding implementations of controls to reduce the initial measurements of franchise risks.

(2) Insurance management, which includes the rewording and management of franchise insurance, which includes both franchisor insurance and franchisee insurance.

This must be done by risk experts independent of any insurers or brokers to ensure the franchise insurance has a high payout ratio, is operationally relevant, and is provided at the most cost effective levels.

Franchise Risk Management

Franchise risk management is a vital component of operating a successful franchise business, helping both franchisors and franchisees identify, assess, and mitigate potential risks.

Effective risk management strategies often involve comprehensive insurance coverage, legal compliance, and operational safeguards to protect against liabilities such as employee accidents, property damage, or legal claims.

Additionally, robust franchise risk management plans ensure compliance with franchise agreements and help maintain brand reputation.

By implementing strong risk management practices, franchisees can minimize financial losses and ensure business continuity in the face of unforeseen challenges.

Case Study on Franchise Insurance

- BeaverTails, a national Canadian franchisor of Food Pastries with over 100 franchisees expanding into the U.S., has been a client of DeshCap since 2015.

- A suite of risk management and franchise insurance services are being provided to BeaverTails on an annual basis.

- This has strengthened their franchise risk management supporting their growth as one of Canada's top brands.

- Our services to BeaverTails include:

- Year-round franchise insurance management encompassing various commercial insurance products;

- Various risk management services to Head Office.

- Our Results to BeaverTails include:

- Consistent optimization of the insurance procurement with high insurance payout ratios;

- Successful claims payouts, expected payouts were received within 90 days, for the franchisor and certain franchisees.

- Minimized franchisor insurance costs year over year for similar protection, and benchmarked against sector related franchise insurance costs.

- Confidence during challenging periods such as business interruption during Covid;

- Supporting franchise business growth and increased market share amidst operational turbulence within the sector.

- The formation, update, and maintenance of a national franchise insurance program including:

- Overseeing the program's insurance broker performance;

- Standardizing protection and insurance compliance across franchisees while minimizing their risks of non-compliance and liability;

- Enabling the best franchisee insurance premiums, year over year, for the large majority of franchisees;

- Enabling risk management and insurance related operational efficiencies for both the franchisor and the franchisees.

- Efforts supporting the enhanced credit risk and investment risk profiles of the company for better financing and valuations.

Frequently Asked Questions

What are Franchise Liabilities?

These include but not limited to the following:

- Liability from a Landlord (ex. not complying with insurance provisions within the lease)

- Liability from an industry body

- Liability from customers (ex. faulty product sold resulting in injury to the customer)

- Liability from shareholders

- Liability from franchisees (ex. franchisees suing a franchisor for misrepresentation)

- Other types of liability risk

Note that each of the above mentioned franchise liabilities can be hedged through different commercial insurance products.

Franchise Insurance Premiums Are Usually high?

Premiums are linked to the type of franchise being insured as well as the dynamics of the general insurance market.

A lot of times a franchised operation can be performing well including having a good insurance claims history, yet still subject to premium increases from insurance brokers and companies.

For example, franchisor insurance premiums have gone up significantly post-covid even if the franchisor had a clean insurance loss history. It is important to utilize advanced analytics in order to maximize on premium negotiations with insurance brokers and companies.

Can a Franchisee sue a Franchisor?

Yes.

Can a Franchise Insurance cover Government Penalties?

Yes.

What is Insurance For Franchise Business?

Typically a franchisor will outline insurance requirements within its franchise agreement (FA) and/or corresponding material.

It is important that a franchisee follow the franchisor insurance requirements in details to minimize compliance risk.

In addition, if the franchised business leases premises then it can be subject to landlord insurance requirements, which also have to be analyzed carefully and mapped against the corresponding franchisor insurance policy.

What are Franchise Insurance Requirements?

Such requirements will vary depending on the type and scope of the franchise amongst other things.

The requirements should be tailored to the nature of the franchise operation including the average size of franchisees.

Franchise insurance requirements should be updated once a year at least to account for changes in the insurance marketplace as well as any changes to the franchise operation itself.

What are Franchise Restaurant Insurance Programs?

Franchise restaurant insurance programs are designed to provide comprehensive coverage tailored to the unique needs of restaurant owners within a franchise system.

These programs typically include general liability, property insurance, workers’ compensation, and business interruption coverage, ensuring that both the franchisee and franchisor are protected from various risks such as food-related incidents, equipment damage, or employee injuries.

Franchise restaurant insurance programs are crucial for maintaining compliance with franchise agreements, which often mandate specific types of coverage to protect the brand and operations.

Having a robust insurance program in place ensures that franchisees can manage risks effectively while meeting legal and contractual obligations.

How can franchise owners reduce insurance costs?

Improving safety controls, conducting risk audits, and standardizing insured practices across locations helps reduce premium.

Who are the national franchise insurance brokers?

There are many national franchise insurance brokers including global household names such as Marsh, Aon, Willis, Lockton as well as regional and local names.

It is important to hire independent insurance consultants to perform tasks outside of the brokers' purview such as claims management and risk-based audit of the fine print. These consultants can also execute on your behalf with national franchise insurance brokers.