Notes on our Business Insurance Premium Calculator

- The Calculator is updated frequently to account for changing variables impacting business insurance premiums.

- It can be used for different purposes including (a) by Insureds to benchmarks their business insurance quotes for better negotiations with brokers; (b) by Brokers to scope out better terms for their clients; (c) by Insurers to gauge market dynamics and improve their business insurance underwriting.

- The Calculator is not an indication of coverage strength.

- The fine print of any policy wording should be reviewed by independent insurance consultants such as our team, which uses the latest analytics to secure lowest business insurance cost for similar tailored coverage - lowest cost contractually guaranteed or else we pay the difference.

For assistance with your procurement of any type of Business Insurance at the lowest cost: Contact DeshCap.

DeshCap is ranked online #1 for Liability Risk worldwide and Top Operational Risk Advisor.

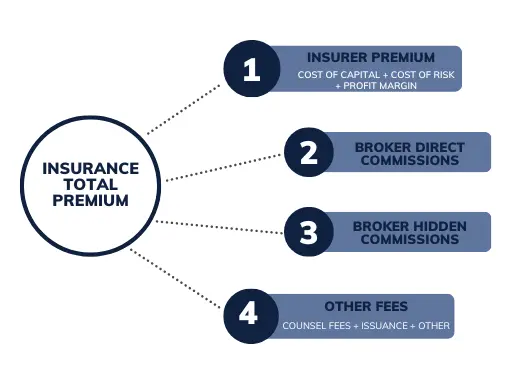

Components of Business Insurance Premium

Variables impacting business insurance premium range from capital markets inputs to decisions made by reinsurers. The following is a brief illustration of the breakdown of business insurance premium.

How Business Insurance Premium is Calculated

As shown above, business insurance premium is made up of several components that dictate the total cost of business insurance.

Each business insurance premium can vary widely depending on a variety of factors, such as the size, complexity, territory, industry, and financials of the business, the type and level of risk involved, the type of business insurance and the requested protection amount, the insurance company's underwriting standards, etc.

Reducing Business Insurance Premiums

Here are a few pointers on steps to take to reduce business insurance premiums:

- Make corporate insurance brokers compete for your business

- Implement operational controls that boost the operational resilience of your business

- Hire independent insurance experts to negotiate on your behalf

If you represent a mid-sized or large company, it is important to understand how to minimize enterprise insurance cost.

Achieving Low Cost Commercial Insurance

Low cost commercial insurance can be achieved even when the insurance market is 'hard'. Independent field experts must be hired to negotiate with brokers effectively. Our team is licensed and pursued post graduate insurance studies making it well positioned to negotiate effectively with brokers and agents.

Contact DeshCap for low cost commercial insurance.

FAQ: Business Insurance Premiums

Why are commercial insurance rates going up?

This is due to 2 factors: 1. the market dynamics; and 2. your ability to negotiate with insurance brokers. It is best to hire a commercial insurance consultant independent of any broker to minimize business insurance premiums.

Why is business insurance so expensive?

See above. Contact us to minimize business insurance cost.

Business Insurance Cost for LLC

Get the lowest business insurance cost for your LLC by analyzing the insurance wording and cutting the fat in it. Contact us to minimize business insurance cost.

General Business Insurance Cost

See above the table showing business insurance premium per product.

How much is a commercial insurance

Please refer to the table above showing the cost of commercial insurance per product.